Since the 1980s, climate-related disasters have gradually ticked up. And the annual dollar cost of disaster losses and recovery has risen 1,580%. This statistic comes from First Street, a firm known for its analyses of climate risks to real estate.

The firm researches the costs of wildfires, storm winds, and water infiltration. In a year with especially severe weather, close to 7% of foreclosure loan losses are likely climate-related.

In a decade, says First Street, climate effects could amount to nearly a third of all mortgage default losses. Wow.

Watch for Lenders to Begin Accounting for the Borrower’s Climate Risk

Credit scorers may start acting on the above facts and projections now, to spare the industry from a growing risk factor. In severe weather years, the lenders of today face somewhere around $1.2 billion in mortgage-related credit losses. And the total, says First Street, could rise to $5.4 billion annually a decade from now. It could, that is, unless companies modify their lending standards.

So, what will this mean for mortgage borrowers?

It means lenders will start looking at our purchases in new ways. Within the rapid rise in climate-related events, lenders are watching the risks to our homes — which, to them, represent loan collateral. If banks trying to assess our credit risk start including climate-related information to protect themselves, then our credit scores could reflect what’s happening in our environment.

How we’re perceived by lenders is essential knowledge for borrowers. Whenever our credit scores take a hit, loans become harder to get, and more expensive when we get them.

Keeping our scores up has always meant using our credit cards and loan products faithfully. But now, it could also involve where we choose to buy, and what we do to address the risks where we buy.

As explained by Matthew Eby, First Street CEO, today’s loan applicant doesn’t just present a set of financial risks to the lender. Now, the homes we buy have their own set of risks. This complicates the question of creditworthiness.

Location, Location, Location: A Classic Phrase Takes on New Meaning

Deed holders in places where disasters are getting more common (and more expensive) are already coping with rising insurance rates — if they are able to get the companies to keep issuing policies at all in these areas.

And as premiums go up to cover the insurers’ positions, homeowners shoulder more of the costs. This is a pain for homeowners everywhere — but especially in hard-hit areas.

When the price of an insurance policy goes up 1%, First Street finds, defaults leading to foreclosure also increase by about 1%.

In short, homeowners stressed out with rising insurance bills may be at risk of going into default. Lenders at that point have to mitigate their losses, so there are ripples throughout the whole real estate financing world.

Even so-called climate havens are dealing with hurricanes and floods these days. See more on The Resilient Deed: What Property Buyers Should Know About Climate, Weather, and Insurance.

Renovations after wildfire or wind damage are normally covered by the homeowner’s insurance policy our lenders make us pay. But of all types of damage across the country, floods are racking up the highest costs. Add to this the rising burden on homeowners as local governments address stormwater runoff.

Drawing on information from the National Oceanic and Atmospheric Administration (NOAA), First Street looked at the risk involved with homes near the coasts. The report found:

- Florida, Louisiana, and California will make up more than half of mortgage lenders’ climate-connected losses this year.

- Foreclosure rates are higher in areas near the coasts or tidal rivers. Flood-related foreclosures outside of official flood zones (where flood insurance is mandatory) are much higher.

Because regular homeowners’ insurance policies don’t cover flood damage, a deed holder might face the entire bill for cleanup. And now the federal government is cutting FEMA’s flood coverage and recovery services, which have long helped people living in disaster areas and flood zones.

Foreclosure by hurricane? Floridians are asking how it’s possible to protect a home deed from the effects of climate losses.

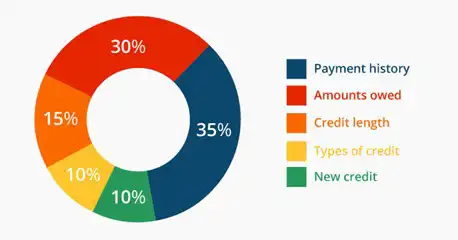

What’s the “6th C” of Creditworthiness? (And What Are the Other 5?)

First Street has titled its new publication The 13th National Risk Assessment: Climate, the Sixth “C” of Credit. Why is Climate the sixth “C”? What are the other five?

Lenders size up borrowers based on a combination of factors. The traditional five aspects of creditworthiness are often outlined this way:

- Character. Essentially, a lender is figuring out whether the loan applicant is more of a saver than a spender.

- Capacity. A lender wants to determine your capacity to repay the loan. To assess this, the lender looks at your dependable income, versus the amount you’ll need to pay off companies every month once you buy the home.

- Capital. The lender wants to know how much you are ready, willing, and able to put on the table up front.

- Conditions. These are the factors surrounding the transaction. They include current interest rates for mortgages, market trends, and other situational factors.

- Collateral. This is what secures the funds a lender is releasing. In this case, the home itself will become collateral.

In some ways, the last two factors do relate to climate impacts. But First Street says climate and related insurance projects should have their own focus — as a sixth C.

Lenders and regulators, says the firm, must adapt their borrower assessment models to account for environmental risks.

Storms can wreak more than physical havoc. They can also affect a deed holder’s rights. Have a look at our Deed Holder’s Intro to Storm Runoff.

A Few Final Words on Where We Are Now

Home loans are “now on the front lines of climate risk,” according to Dr. Jeremy Porter of First Street. First Street models show that doing nothing is out of the question. If lenders don’t take climate-related impacts into account, their default losses will snowball.

The new “Sixth C” report illustrates the impact of weather disasters on the value of collateral, both from direct damages, and indirect drivers. The indirect costs include rising insurance and renovation bills, and the erosion of market values after disasters become public knowledge.

So, change is coming. People who make decisions about loan applicants will soon focus on climate risk if they aren’t doing so already. Home buyers ourselves can help manage risk. Part of this will involve buying strong homes, built to resist damage. Considering the “six Cs” is key to preparing for the market ahead of us.

Supporting References

First Street: The 13th National Risk Assessment – Climate, the Sixth “C” of Credit (May 19, 2025).

Eric C. Peck for The MortgagePoint: Climate Risk Emerges as New Mortgage Credit Metric, Study Finds (May 19, 2025).

Diana Olick for CNBC LLC, a division of NBCUniversal, via CNBC.com: Need a Home Mortgage? Here’s How Climate Change Could Hit Your Credit Score (May 19, 2025).

CapitalOne via CapitalOne.com: What Are the Five Cs of Credit? (Feb. 8, 2024).

And as linked.

More on topics: Risks of deeds in wildfire country, AI and climate-smart construction

Photo credits: Photo by Yaroslav Shuraev via Pexels/Canva and CafeCredit / Flickr (CC BY-SA 2.0).