Category: Mortgage

-

Does a Quitclaim Deed Remove You From the Mortgage?

No. A quitclaim deed transfers your interest in the property’s title. It does not change who is responsible for paying the loan. Those are two separate legal instruments, and signing one has no automatic effect on the other. This distinction trips up a lot of people — especially during divorce, family transfers, or buyouts between…

-

Lien Release: Getting Ready for Your Final Mortgage Payoff (Woohoo!)

Are you closing in on the day you finish paying off the entire mortgage? Or just wondering what that finish line looks like? What steps do you need to take to get that lien off, and own the home free of debt? Let’s take a look.

-

Risky Business: “Subject to Mortgage” Sales Leave Floridians With Debt and No Deed

In Jacksonville, News 4 just ran an I-Team investigation on homes being sold subject-to a mortgage. These so-called sub-to deals are gambles, said the reporter. A sub-to real estate deal could be a valid method of selling your home in some situations. But this approach carries serious financial risks. Here, we look at how that…

-

Mortgage Fraud Risk Rises, as White House Moves to Banish the Watchdog

Mortgage applications with signs of fraud have increased more than 8% since this time last year. The news comes from the property analytics firm Cotality. The firm runs algorithms through applications, pinpoints possible fraud, and maintains the National Mortgage Application Fraud Risk Index. Cotality notes that real estate fraud rises as more investors take out…

-

If I Have a Mortgage, Who Really Holds the Title to My Home?

A home buyer who uses financing — as most people do — is considered a homeowner, as opposed to a renter. The buyer has paid the seller, so the buyer owns the home, regardless of whether the deal is done with cash or financed. If the property’s value rises (or falls), then the gain (or…

-

Federal Reserve Poised to Start Rate Cuts: What’s Next for Mortgages?

Mortgage rates are dipping down in advance of the Federal Reserve’s discussion of rate cuts this week. Freddie Mac shows the average rate on 30-year, fixed-rate home loans is just about 6.3% as of mid-September, down from 7% at the start of 2025. Two weak U.S. employment reports pushed the average rate down. In response,…

-

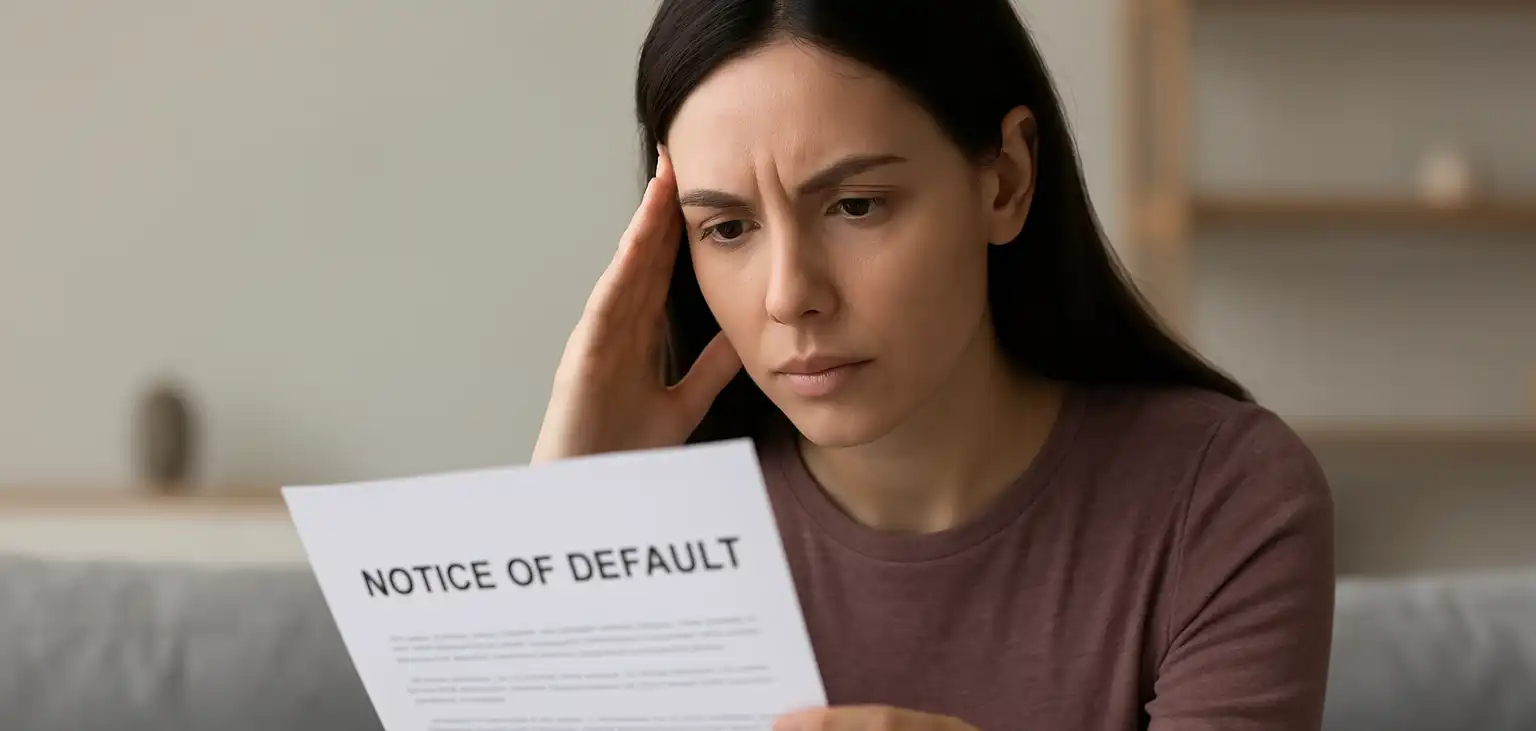

Q & A: Why Did I Get a Notice of Default on the Mortgage?

It’s that time of year again. Mortgage holders’ bank accounts face extra stress in many households. The 2024 tax bills are now due. So are estimated 2025 taxes for small business owners. When taxes are done, what if insufficient funds remain for the mortgage payment? Mortgage lenders send a notice of default (a.k.a. notice of…

-

Does Starting a Mortgage Later in Life Make Sense?

Some older adults might wonder. They also might wonder if the bank will want to lend to them. There are plenty of good reasons for older adults to buy homes. People over 60 make up about a third of the population of home buyers. That’s because starting a mortgage and acquiring a deed can be…

-

Looking for a Path to Homeownership? Look Again at Down Payment Assistance.

The typical person can’t afford the typical home. As property values keep rising, down payments aren’t getting any easier to make. If you know the feeling, have you looked up down payment assistance? It can be a grant, with no repayment requirement. Or it could be a loan — possibly a forgivable loan. Even if…

-

What Resources Exist for Deed Holders Who Need Cash?

Ever heard the phrase house rich, cash poor? It can be frustrating to have a valuable home and empty pockets. You might be dealing with job changes, emergencies, new goals, hopes and dreams… And you need cash. Can you reach into your property value to get the cash now — without downsizing to a cheaper…

-

Troubleshooting After Divorce: My Name Is Still on My Ex’s Mortgage.

Maybe your ex got your former home through your divorce. And maybe you thought it made sense to let your ex keep the loan — after all, the interest rate on it is great! And those are your kids living in the home… why make life harder for them by complicating the status of the…

-

Borrowing Against Your Equity: HELOCs, Home Equity Loans…and Interest Rates

One of the opportunities you have as a deed holder is the ability to borrow against the home equity you build over the years. But wait. How high is the interest rate you’ll have to pay? Is it worthwhile to pay that rate, in light of what the funds you borrow can do for you…

-

Tapping Into Home Equity Puts a Lien on Your Deed. Consider the Risks.

Many deed holders have accumulated a lot of home equity over recent years. Financial gurus online often encourage homeowners to tap into it. After all, why not take advantage of a home’s rise in value to get cash and do something on your bucket list? But handy as they are, home equity loans do come…

-

I’m a Senior, Looking for a Mortgage. Will I Be Treated Fairly?

Great question. The first thing to know is that the Equal Credit Opportunity Act is on your side! Under this federal law, lenders may not consider an applicant’s age as a reason to approve or turn down your application. Simply stated, seniors can get mortgages if they demonstrate their ability to make the monthly mortgage…

-

The Rise and Rise of Down Payments

A down payment is the portion of a home’s purchase price the mortgage borrower pays upfront. You knew that. But did you know the median down payment for U.S. homebuyers is now more than $55K+? That’s remarkable. It was less than $45K just last year. Buyers often try to put 20% of the purchase price down.…