So many people need answers. What states are attracting the most home seekers at this time? What states are now the best bets for people who hope to save for a mortgage? Is it even worthwhile, now, to try to get positioned to buy a home?

Let’s see where buyers are looking, where saving for a down payment is possible, and whether it even makes sense to try.

Trend Shift: More People Are Moving to South Carolina Than Texas

People are now moving into South Carolina more than anywhere else. That means South Carolina has jumped ahead of Texas as the country’s top destination state for home seekers.

So, Texas is now #2. North Carolina is now the third most sought-after state for home seekers. And Florida now comes in fourth.

So, where are people coming from? New Yorkers make up the biggest group of households relocating to South Carolina — a total of 5,476 in 2024.

In general, over the past five years in a row, people have been leaving California the most. After that, people left Massachusetts most. And New Jersey had the third biggest exodus last year.

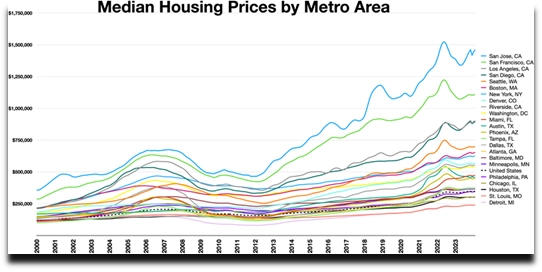

In This Market, Does It Really Make Sense to Chase the Dream of Homeownership?

Hopeful buyers might look at the staggering cost of homes and think the market must be headed for a downfall. But if you’re anticipating housing to crash — or even to dip — think again.

Five years ago, the median home sale brought $296K. It’s up 44% since then, with the median home price now having reached $427K. Some popular types of homes doubled in value in just the past five years.

At this point, the number of available homes is expanding, and that’s helping to keep prices in check. But more inventory certainly isn’t equating to lower prices.

Home prices are currently up 6.3% year-over-year. In 2025, housing prices can be expected to continue their upward climb. The price of the median home could rise 3% according to many forecasts.

It all goes back to one constant. In the long run, the worth of home properties goes up. When in doubt, zoom out and you’ll see a continuous pattern, despite short-term dips, spikes, and distractions. Trying to time the market is difficult and may be futile. If you’re fortunate enough to find the right home at a fair price, it’s the right time.

Demand is strong, and one in every four homes for sale fetches more than its listed price. While you don’t want to rush in and overpay for a home, you’ll need to be careful that trying to negotiate doesn’t cause you to lose out on a good home.

So, Where Are the Easiest Markets to Save Up for the Deed to a Home?

Different states have different levels of challenges for the home seeker.

CNBC.com cites a report by the investment company RealtyHop. The company sets out to rank the financial “barrier to homeownership” for the median home for sale in cities across the country. Say a household can set aside 20% of its annual gross income. How many years would it take for that household to amass funds for a 20% down on that home?

Here goes:

- It would take more than a decade in New York City to save up 20% of the median $865K home.

- The median list price for homes in Los Angeles exceeds a million dollars. A typical L.A. household would be socking away cash for 14 years to gather a 20% down payment.

- Beyond Los Angeles and New York City, major barriers to homeownership belong to Miami, and two other California cities: Irvine and Anaheim. Of these cities, Miami would be cheapest, but the median home there is still a whopping $700K.

- It could take just two and a half years for a household in Detroit to finish gathering a 20% down payment for the median-price home for sale. That would be $20K down for a $100K home. Detroit’s median household income is just under $40K.

- Four other cities would allow for a household to get a mortgage in under four years. A buyer in Cleveland, where the typical home costs $139K, would need to save up just $28K. Buyers could also do it in under four years in Baltimore, Buffalo, or Pittsburgh. A home in Pittsburgh typically costs just a third of a Miami home’s price.

Even trying to set money aside for two years is easier planned than done for much of the U.S. population. For a third of us, credit card debt is growing faster than we can keep savings in reserve. A fourth of us have no savings.

Plus, even in low-barrier cities, saving is much harder for households raising kids.

But Is 20% Down Necessary? Why or Why Not?

It’s not required. If you can come up with about $30K, you can make a normal down payment. At this time, per the National Association of REALTORS®, people are putting 14% to 15% down on average. If you can’t swing that, consider these loan options:

- A VA loan from the U.S. Department of Veterans’ Affairs. In theory you can buy a home with a VA loan with no money down. The terms of your VA loan will depend on your unique financial profile.

- A USDA loan from the Department of Agriculture. In theory you can use the USDA loan to buy a home with no money down, and buyers in a surprisingly large area of the nation are eligible. Curious? Check out what counts as a rural area for the purpose of a USDA mortgage.

- The very popular FHA loans from the Federal Housing Administration. You might get one of these for as little as 3.5% down.

Of course, the less money you put down for closing, the bigger the debt you’ll take on.

And another thing: PMI. The lender tacks on the cost of private mortgage insurance to the monthly mortgage charge if a borrower intends to put less than 20% down on a home. This could add thousands of dollars a year to the borrower’s obligation.

You might be wondering… “Should I accept PMI if there’s no other way to buy a home? Can I get out of it later, once I’ve paid off 20% of my home?” Take a look at our Guide to Private Mortgage Insurance to learn more.

Down Payments Aren’t Everything: A Few Other Costs to Keep in Mind

Closing costs for the loan tend to range in the area of 5% of the total borrowed, more or less. Factor them in. And look into more potential costs of acquiring a deed that you might not have considered.

Interest rates will also impact the buyer in 2025. With inflation back in play, new federal interest rate cuts are unlikely for the first half of 2025. After that, rates could ease slightly. Watch this space.

Supporting References

Brian Kim, CPA for ClearValue Tax, via YouTube.com: 2025 Housing Market Update – Prices, Rates & Predictions (Jan. 20, 2024).

Ana Teresa Solá for CNBC LLC (part of NBCUniversal) via CNBC.com: Five Cities With the Lowest “Barrier to Homeownership” Where Saving a 20% Down Payment Takes Less Than Four Years (Jan. 19, 2025).

Jaclyn DeJohn, CFP® for SmartAsset via NASDAQ.com: People Are Moving to South Carolina From These Places – 2024 Study (Oct. 30, 2024).

And as linked.

More on topics: Where people are struggling most with housing costs, NAR predicts no housing crash

Photo credits: Cottonbro Studio via Pexels/Canva; and Zillow, via Wikimedia Commons / Public Domain.