Mohave County Disclaimer of Interest Form

Last validated July 22, 2026 by our Forms Development Team

Mohave County Disclaimer of Interest Form

Fill in the blank form formatted to comply with all recording and content requirements.

Mohave County Disclaimer of Interest Guide

Line by line guide explaining every blank on the form.

Mohave County Completed Example of the Disclaimer of Interest Document

Example of a properly completed form for reference.

All 3 documents above included • One-time purchase • No recurring fees

Immediate Download • Secure Checkout

Additional Arizona and Mohave County documents included at no extra charge:

Where to Record Your Documents

County Recorder

Kingman, Arizona 86401 / 86402

Hours: Monday thru Friday 9:00 am until 5:00 pm

Phone: 928-753-0701

Recording Tips for Mohave County:

- Ask if they accept credit cards - many offices are cash/check only

- Avoid the last business day of the month when possible

- Make copies of your documents before recording - keep originals safe

- Both spouses typically need to sign if property is jointly owned

Cities and Jurisdictions in Mohave County

Properties in any of these areas use Mohave County forms:

- Bullhead City

- Chloride

- Colorado City

- Dolan Springs

- Fort Mohave

- Golden Valley

- Hackberry

- Hualapai

- Kingman

- Lake Havasu City

- Littlefield

- Meadview

- Mohave Valley

- Oatman

- Peach Springs

- Temple Bar Marina

- Topock

- Valentine

- Wikieup

- Willow Beach

- Yucca

Hours, fees, requirements, and more for Mohave County

How do I get my forms?

Forms are available for immediate download after payment. The Mohave County forms will be in your account ready to download to your computer. An account is created for you during checkout if you don't have one. Forms are NOT emailed.

Are these forms guaranteed to be recordable in Mohave County?

Yes. Our form blanks are guaranteed to meet or exceed the applicable formatting requirements used for recording in Mohave County, including margin requirements, font requirements, and other layout standards. This guarantee applies to formatting, not to the legal sufficiency of information entered by the user or the suitability of a form for a particular transaction.

Can I reuse these forms?

Yes. You can reuse the forms for your personal use. For example, if you have multiple properties in Mohave County you only need to order once.

What do I need to use these forms?

The forms are PDFs that you fill out on your computer. You'll need Adobe Reader (free software that most computers already have). You do NOT enter your property information online - you download the blank forms and complete them privately on your own computer.

Are there any recurring fees?

No. This is a one-time purchase. Nothing to cancel, no memberships, no recurring fees.

How much does it cost to record in Mohave County?

Recording fees in Mohave County vary. Contact the recorder's office at 928-753-0701 for current fees.

Questions answered? Let's get started!

The Arizona Disclaimer of Interest is the instrument a beneficiary uses under the Arizona Uniform Disclaimer of Property Interests Act at ARS 14-10001 et seq. to refuse all or part of an interest in property the beneficiary would otherwise receive — typically an inheritance, a survivorship interest, a beneficiary deed transfer, or a distribution from a trust. A valid disclaimer causes the disclaimant to be treated as though they had predeceased the decedent or never received the interest, with the property passing to whoever would have taken if the disclaimant had not existed. The timing is unforgiving: under ARS 14-10005, the disclaimer must be made before the beneficiary has accepted the interest or exercised dominion over it, and for tax-qualified disclaimers under federal law, it must be delivered within nine months of the interest-creating event. Once executed, a disclaimer is irrevocable — the decision cannot be undone — which is why the drafting and timing matter.

When the Arizona Disclaimer of Interest Is Used

Disclaimers are used in several common scenarios. Estate tax planning is one driver: a surviving spouse may disclaim a portion of the decedent's estate to route it directly to the children or to a credit-shelter trust, reducing the combined estate tax exposure at the second death. Asset protection is another: a beneficiary facing creditor pressure may disclaim an inheritance to prevent it from becoming reachable by creditors, though the effectiveness of this strategy depends heavily on timing relative to creditor claims and on specific state and federal rules. Beneficiary correction is a third: when a decedent's plan has become outdated (an intended charitable beneficiary no longer exists, a named individual has become unsuitable, an unequal distribution no longer fits family circumstances), a disclaimer can redirect property to beneficiaries who would take by default under the will, trust, or intestacy statute. Disclaimers are also used in blended-family situations to route property to stepchildren or former spouses in ways the original plan did not contemplate, and in Medicaid-eligibility situations where accepting an inheritance would disqualify a beneficiary from benefits (though Medicaid-driven disclaimers are scrutinized under separate federal rules that may treat the disclaimer as a transfer for purposes of eligibility).

The "No Acceptance" Rule Under ARS 14-10013

A fundamental constraint on disclaimers is that they are not available if the beneficiary has accepted the interest. Under ARS 14-10013, a beneficiary who has accepted an interest — by taking possession, receiving a distribution, exercising ownership rights, or pledging the interest as collateral — has lost the ability to disclaim it. The policy is that disclaimers must be true refusals, not retroactive regret; once a beneficiary has treated property as their own, they cannot later pretend they never received it.

What counts as "acceptance" is sometimes subtle. Taking physical possession of a bequeathed item is acceptance. Receiving a check from a trust distribution and depositing it is acceptance. Making demands on a fiduciary for an accounting or for specific distributions is typically acceptance as to the interest demanded. Residing in inherited real property for an extended period can constitute acceptance. Signing documents that treat the interest as the beneficiary's own — deeds, contracts, tax returns reflecting ownership — is acceptance. By contrast, mere passage of time without action typically does not constitute acceptance; a beneficiary can take several months (up to the statutory disclaimer period) to evaluate whether to disclaim without that passage of time being treated as acceptance, provided no affirmative steps toward ownership have occurred. When a beneficiary is uncertain whether particular actions might foreclose the disclaimer option, erring on the side of doing nothing while the disclaimer decision is being evaluated is the safer approach.

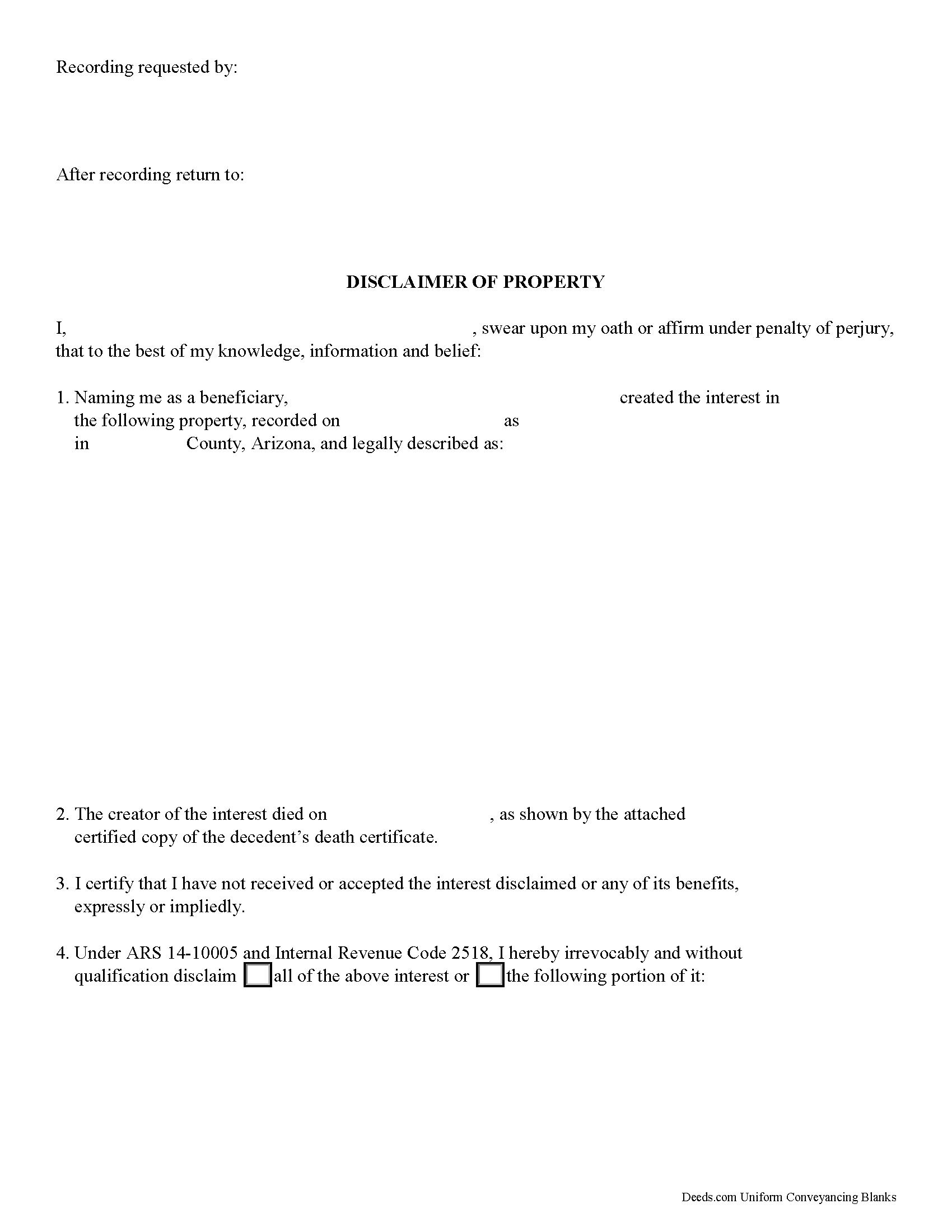

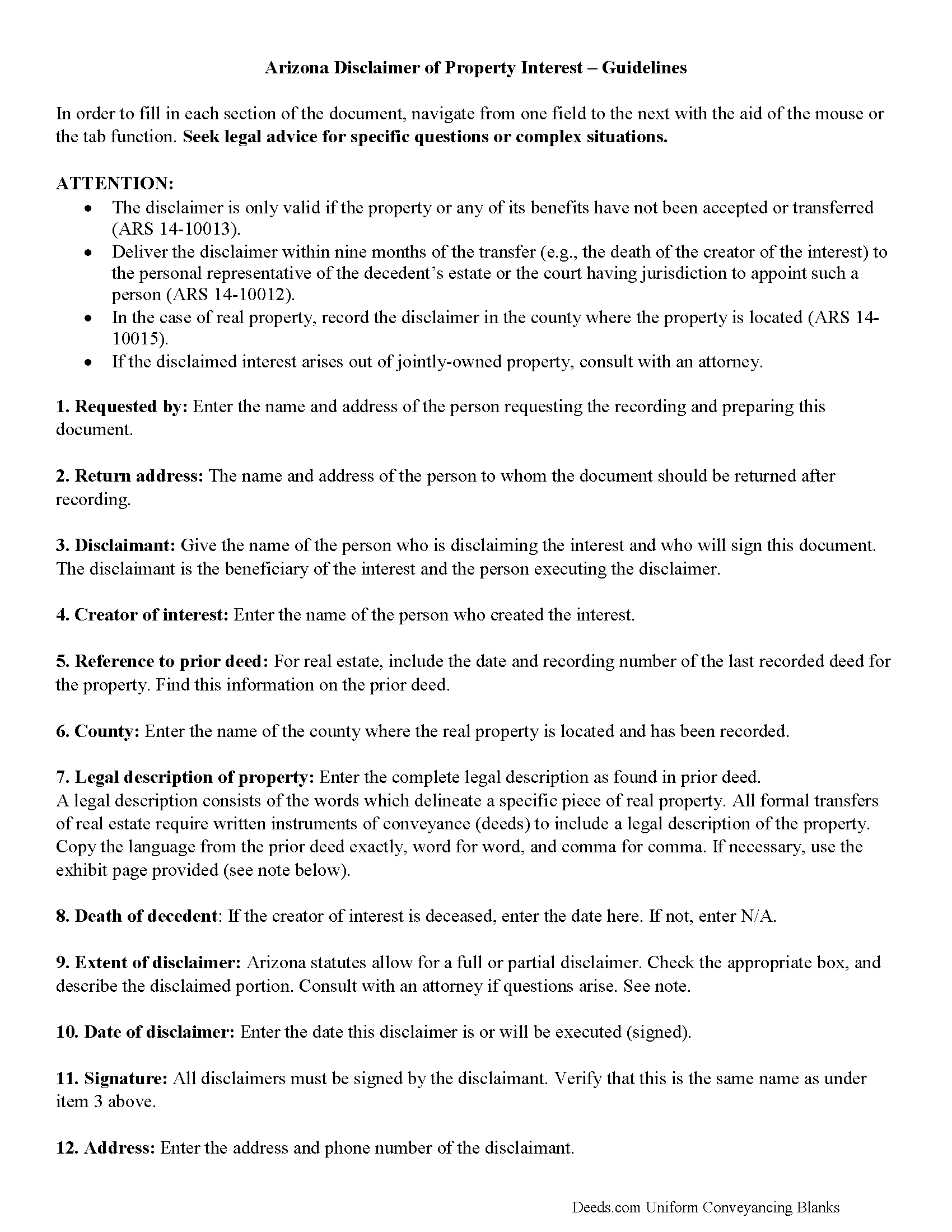

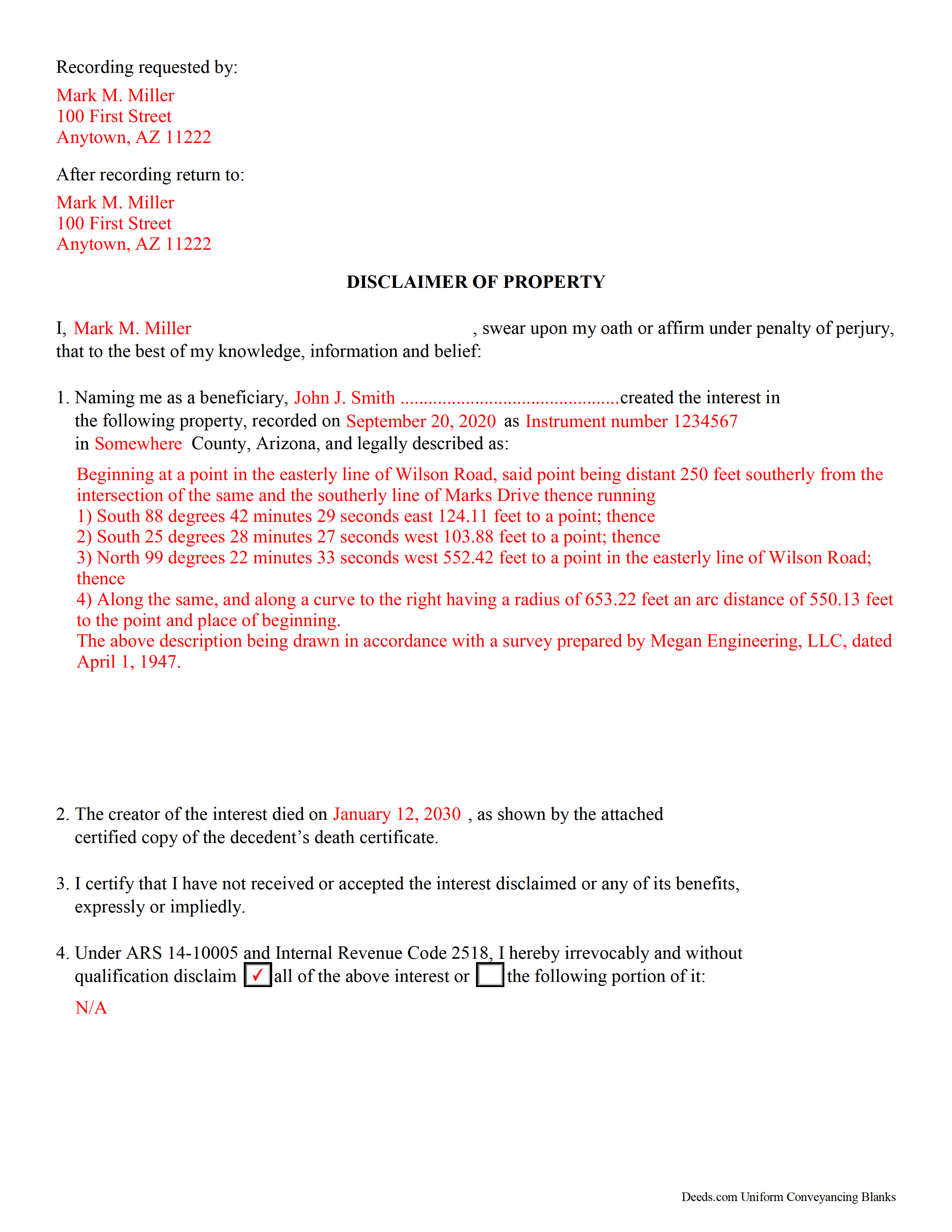

Content of the Disclaimer — ARS 14-10005(C)

The disclaimer is a written instrument with specific content requirements. Under ARS 14-10005(C), the document must describe the interest being disclaimed with sufficient specificity to identify what is refused, declare the disclaimant's intent to disclaim the interest (either in whole or in the defined portion being refused), and be signed by the disclaimant. For a disclaimer affecting real property, the description should include the property's legal description, the source of the disclaimant's interest (the will, the trust, the beneficiary deed, the joint tenancy, or the intestacy statute), and enough detail that the relationship between the disclaimer and the source of the interest is clear. Partial disclaimers need particular precision — disclaiming "half" or "a 25 percent interest" or "all but the homestead exemption" is meaningful only if the resulting fractions or categories are defined with enough specificity that the outcome is unambiguous.

The Nine-Month Timing Rule

ARS 14-10012 and related provisions, together with federal tax law under Internal Revenue Code Section 2518, establish the timing framework for disclaimers. A qualified disclaimer under federal law — which is the standard most Arizona practitioners target to preserve tax benefits — must be made within nine months of the transfer that creates the interest. For interests arising on death, the nine-month period runs from the date of death. For interests arising from a beneficiary designation that was already in place when the disclaimant had capacity to disclaim (for example, the disclaimant was born named as a beneficiary of an irrevocable trust), the period can run from when the disclaimant reached the age at which they could have exercised the interest, or from events later in the chain, depending on the specific circumstances.

Arizona state law may permit a longer disclaimer period for non-tax purposes in certain circumstances, but the nine-month federal deadline is usually controlling because the disclaimant typically wants the tax consequences to flow through properly. A disclaimer executed after the nine-month period may still be effective under state property law — redirecting the interest to whoever takes by default — but may not qualify for the federal tax treatment, which can be a material difference for significant-value interests. Timing should be evaluated as of the triggering event, not the date the disclaimant learned about it: inheritance can be delayed in reaching the beneficiary, but the clock started running at death regardless.

Who Takes After the Disclaimer

A disclaimer does not let the disclaimant choose who receives the property — it simply redirects the property according to the rules that would have applied if the disclaimant had predeceased the decedent or never received the interest. For a disclaimed devise under a will, the property passes to the residuary beneficiary if the devise was specific, or to the alternate devisees if the will names them, or to the intestacy heirs if no alternate is specified. For a disclaimed inheritance under the intestacy statute, the property passes to the next heirs in the statutory order, which typically means to the disclaimant's descendants. For a disclaimed beneficiary deed transfer, the property passes to any successor beneficiaries named in the deed, or back into the decedent's probate estate if no successor is named. For a disclaimed distribution from a trust, the property passes according to the trust's default provisions for when a beneficiary is unavailable.

The disclaimant needs to think carefully about where the property actually ends up before executing the disclaimer. A disclaimer intended to benefit the disclaimant's children will succeed if the children are the takers by default, but will fail (and send the property somewhere unintended) if the document's default provisions direct property elsewhere. Reviewing the will, trust, or beneficiary deed to confirm where disclaimed property actually goes is a required step before signing.

Special Considerations for Jointly Owned Property

Disclaimers of interests in jointly owned property have particular complexity. When a joint tenant dies and the surviving joint tenant wishes to disclaim, the analysis involves whether the disclaimer can reach all or part of the survivor's interest or whether the survivor's interest is already considered "accepted" by virtue of the joint tenancy itself. Federal tax law has developed specific rules for qualified disclaimers of joint interests that distinguish between interests that pass by right of survivorship (potentially disclaimable within nine months of the joint tenant's death) and interests in property the disclaimant already owned during the joint tenancy (often treated as already accepted at the time of joint tenancy creation). Arizona community property creates additional layers, because the community property and community property with right of survivorship vestings have their own rules for which half-interest passes at the first death and how it can be disclaimed. Disclaimers in joint-ownership contexts almost always warrant specific legal advice, because the wrong assumption can produce an ineffective disclaimer or unexpected tax consequences.

Filing and Recording Requirements

ARS 14-10012 requires filing the disclaimer with the probate court — typically the court in the county where the estate is being administered, or where the estate would be administered if no probate is currently open. For disclaimers of real property interests, ARS 14-10015 requires the disclaimer to be acknowledged as a deed would be and recorded with the county recorder in the county where the property is located. This dual filing-and-recording requirement distinguishes disclaimers of real property from disclaimers of other interests (which are typically only filed with the probate court), and the recording requirement is what puts the disclaimer into the chain of title so future purchasers and title examiners can see the redirection.

The disclaimer should also be delivered to the fiduciary or other party currently holding custody or possession of the property — the personal representative of an estate, the trustee of a trust, the escrow agent holding a beneficiary deed closing, or the other party to a joint tenancy. Delivery to the fiduciary is what starts the clock on the property moving to the alternative recipient, and it also eliminates any argument that the fiduciary was unaware of the disclaimer and could proceed with a distribution to the disclaimant.

Irrevocability

Once executed and delivered, a disclaimer is irrevocable. A disclaimant cannot change their mind on learning new information, discovering the property was more valuable than expected, or reconsidering the estate plan. The property has passed to the alternative recipient, and the disclaimant's only recourse is to request that recipient voluntarily transfer the property back — which is entirely at that recipient's option and which, if it occurs, is treated as a new gift from that recipient to the disclaimant for tax purposes, not a retroactive reversal of the disclaimer. The irrevocability rule exists because the disclaimant's choice has third-party consequences; alternative recipients are entitled to rely on the disclaimer and to make their own planning decisions based on what they now own.

Execution and Acknowledgment

For a disclaimer affecting real property, the instrument must be signed by the disclaimant and acknowledged before a notary public, with the execution requirements tracking those of a deed under ARS 33-401. Arizona does not require subscribing witnesses. When the disclaimant is an individual, the signature is straightforward. When the disclaimant is a fiduciary disclaiming on behalf of an incapacitated beneficiary, additional authority may be required — disclaimers by guardians, conservators, or attorneys-in-fact are permitted under Arizona law but typically require specific authorization from the governing instrument or from a court order, because a disclaimer is a decision with significant consequences and the ordinary presumption is that the beneficiary's fiduciary is obligated to accept property on the beneficiary's behalf rather than refuse it.

Formatting and Recording

ARS 11-480 sets the formatting requirements for every recordable instrument: legible type of at least ten points, white paper no larger than 8.5 by 14 inches, a caption identifying the document (for example, "Disclaimer of Interest"), a top margin of at least two inches on the first page reserved for the recorder's stamp, and minimum half-inch margins elsewhere. Record the disclaimer with the county recorder in the county where the real property is located, and file the same disclaimer (or a certified copy) with the probate court as required by ARS 14-10012. Confirm current recording fees and accepted forms of payment with the county recorder and probate court in advance.

What's Included in the Download Package

The Arizona Disclaimer of Interest package includes the disclaimer form drafted around the Arizona Uniform Disclaimer of Property Interests Act at ARS 14-10001 et seq. with the content required by ARS 14-10005 and execution formalities suitable for recording under ARS 14-10015, detailed guidelines covering the Arizona-specific drafting, timing, and dual filing requirements, and a completed example showing how the form should look for a typical disclaimer of a real property interest. All files are available for instant download after purchase.

Important: Your property must be located in Mohave County to use these forms. Documents should be recorded at the office below.

This Disclaimer of Interest meets all recording requirements specific to Mohave County.

Our Promise

The documents you receive here are guaranteed to meet or exceed the applicable Mohave County recording format requirements. If there is a rejection caused by our formatting, we will correct the issue or refund your payment. This guarantee applies to document formatting only and does not extend to information entered by the user, the selection of the form, or the legal effect of the completed document.

Save Time and Money

Get your Mohave County Disclaimer of Interest form done right the first time with Deeds.com Uniform Conveyancing Blanks. At Deeds.com, we understand that your time and money are valuable resources, and we don't want you to face a penalty fee or rejection imposed by a county recorder for submitting nonstandard documents. We constantly review and update our forms to meet rapidly changing state and county recording requirements for roughly 3,500 counties and local jurisdictions.

4.8 out of 5 - ( 4767 Reviews )

Timothy C.

January 6th, 2022

The process was all very clear and easy -- pay the fee online and download the state and county forms onto my computer. I will do as instructed for the Revocable Transfer on Death Deed, then update my review after I file this with the office of the Sandoval County (New Mexico) Clerk.

We appreciate your business and value your feedback. Thank you. Have a wonderful day!

James T.

July 12th, 2021

Very easy to use. Straightforward and informative

Thank you for your feedback. We really appreciate it. Have a great day!

Kenneth K.

October 8th, 2019

It was fast and easy to use.

Thank you!

Kathryn C.

April 20th, 2022

descriptions for some areas were longer than what would print out on document - it showed and was visible on the form but would not print out - for example in the legal description. would be nice in fill in areas could be extended as needed

Thank you for your feedback. We really appreciate it. Have a great day!

Lisa C.

December 5th, 2023

Thank you. Very easy!

We are delighted to have been of service. Thank you for the positive review!

Amber H.

January 31st, 2019

after typing in the information, the printing is not in alignment - looks disorganized on the page and hard to read

Thank you for your feedback. We will flag the document for review.

Byron M.

March 10th, 2022

This is a great service and a time saver for the company. We get fast responses and a detailed explanation if something additional is needed.

Thank you for your feedback. We really appreciate it. Have a great day!

Ondina S.

December 28th, 2021

Am very happy with the wealth of forms that were available with my purchase! This site is an awesome resource which I plan to use in the future.

We appreciate your business and value your feedback. Thank you. Have a wonderful day!

Rebecca F.

November 4th, 2021

Forms were great. I wasn't able to find them anywhere. Even the county recorder didn't have them

Thank you for your feedback. We really appreciate it. Have a great day!

Jamie F.

February 13th, 2019

I purchased he Alabama Correction Warranty Deed Form to correct a mistake in the legal description. However, this form says it must be signed by all who previously signed the deed. One of these people is now deceased. Can I use this form? How would it be different? I would give you 5 stars but wish this issue had been addressed. Thanks.

Thank you for your feedback. From the product description: All parties who signed the prior deed must sign the correction deed in the presence of a notary.

Laurie R.

August 31st, 2022

FIVE STARS !!! Clear instructions Easy to navigate Thanks for making this easy for those of us who are not tech savvy

We appreciate your business and value your feedback. Thank you. Have a wonderful day!

John H.

October 13th, 2019

works nice

Thank you!

Joel M.

November 8th, 2024

Very easy and efficient. The team was quick to respond when I had questions and made it very simple.

We are delighted to have been of service. Thank you for the positive review!

Randy T.

January 22nd, 2019

I gave your site and forms 5 stars because it is very easy to use and included all the information needed to complete the form without having had a legal background.

Thank you Randy. Have a great day!

SHIRLEY R.

August 22nd, 2019

This was Awesome!

We appreciate your business and value your feedback. Thank you. Have a wonderful day!