Arizona Gift Deed

County Specific Legal Forms Validated as recently as July 24, 2026 by our Forms Development Team

About the Arizona Gift Deed

How to Use This Form

- Select your county from the list on the left

- Download the county-specific form

- Fill in the required information

- Have the document notarized if required

- Record with your county recorder's office

What Others Like You Are Saying

"Love it"

"I had an issue due to the fact that I had many beneficiaries. I was and still am not sure how to han…"

"Appreciated the prompt answers to my inquiries…"

"So quick and easy"

"Very responsive and helpful. Made a big task quite easy and effecient. I would highly recommend. Rea…"

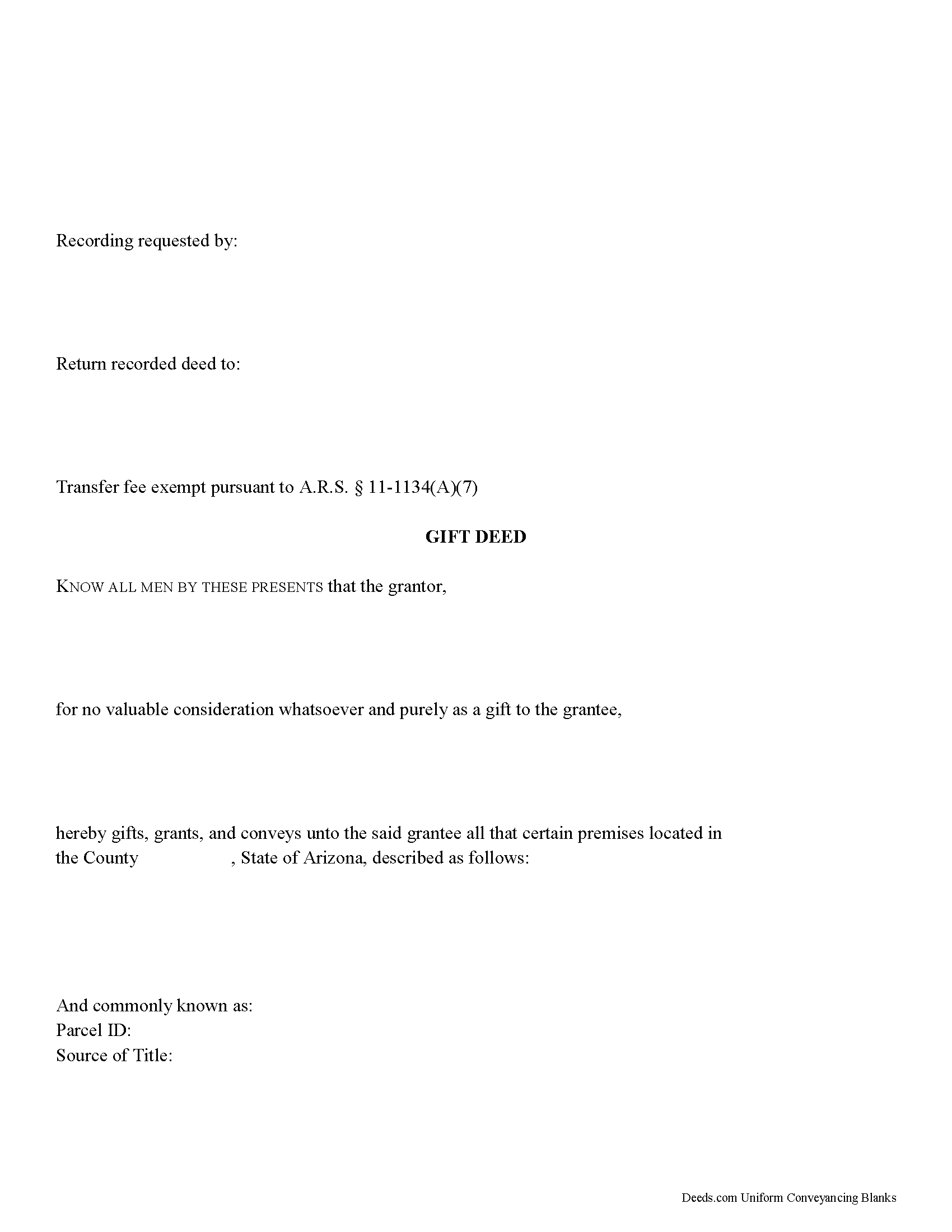

The Arizona Gift Deed form conveys real property from a donor to a recipient without consideration, typically between family members or to a charitable organization. Arizona's treatment of gift deeds differs from many states in two practically important ways: gifts of real property are exempt from both the real estate transfer fee and the Affidavit of Property Value that accompany nearly every other deed under ARS 11-1133, and — critically in this community property state — real property gifted to a married grantee is not presumed to be community property. Those two rules shape how the deed is drafted, what supporting paperwork is required at recording, and what each spouse actually owns after the transfer.

When the Arizona Gift Deed Is Used

A gift deed is used for lifetime transfers that carry no exchange of consideration — no money, no assumption of debt, no trade of other property, nothing of value flowing back to the donor. Common uses include transfers from a parent to a child, transfers to a grandchild or sibling, transfers to a charitable or religious organization, and transfers into a revocable living trust when the settlor is funding the trust as a gift rather than for value. Because consideration is the feature that distinguishes a gift from a sale, the deed must expressly state that the conveyance is made without consideration; ambiguous or placeholder recitals such as "for ten dollars and other valuable consideration" defeat the gift character and can leave the transfer contestable later.

Implied Covenants Under ARS 33-435

Arizona attaches implied covenants of title to any deed that uses the operative words "grant" or "convey" (ARS 33-435). By using those words, the grantor represents that the estate is free from encumbrances made by the grantor and that the grantor has not previously conveyed the same interest to another party. These covenants carry the same legal effect as if they were written out on the face of the deed, and they apply to gift deeds just as they apply to sales. A donor who wants to convey without any implied covenants — passing only whatever interest the donor happens to hold — should use a quitclaim deed instead, because the implied covenants under 33-435 travel with the grant language and cannot simply be waived by silence.

Community Property and the Gift Exception

Arizona is a community property state, and the default rule is that property acquired by either spouse during marriage is community property of both spouses (ARS 25-211). Gifts are the headline exception: real property acquired by one spouse during marriage by gift, devise, or descent is that spouse's separate property, not community property. This means a parent who gifts a home to an adult child does not, by default, also give an interest to the child's spouse — even though the couple is married and even though the child later uses the property as a marital residence. The separate-property character is preserved only if the deed is drafted to reflect it and the recipient does not subsequently commingle or transmute the property into community property.

To preserve the separate-property character on the record, the grantee's vesting clause should read, for example, "to [Grantee], a married person, as her sole and separate property." Many transactions also record a contemporaneous disclaimer deed from the non-recipient spouse to eliminate any community property presumption in the chain of title. Getting this right at the time of the gift is materially easier than fixing it later, because a muddled vesting clause invites disputes in divorce and in estate administration.

Vesting Options for the Grantee

Arizona recognizes several forms of co-ownership beyond sole ownership: tenancy in common, joint tenancy with right of survivorship, community property, and community property with right of survivorship (ARS 33-431). A conveyance to two or more grantees without a specified tenancy vests as tenancy in common by default. Joint tenancy and community property with right of survivorship are available only when expressly stated in the granting clause, and community property forms are available only to married grantees. When a donor is gifting to multiple recipients — siblings, grandchildren, a child and the child's spouse — the vesting clause controls what happens on the death of one co-owner and should be chosen deliberately, not left to the statutory default.

Execution and Acknowledgment

Under ARS 33-401(B), a conveyance of real property must be signed by the grantor and acknowledged before a notary public or other officer authorized to take acknowledgments. Arizona does not require subscribing witnesses on a deed. When the deed is signed outside Arizona, the acknowledgment must comply with the rules for out-of-state acknowledgments, and the officer's certificate must satisfy Arizona's formal requirements. The grantor's full name, marital status, and mailing address belong in the instrument, along with the grantee's full name, marital status, mailing address, and chosen vesting.

Exemption from the Affidavit of Property Value and Transfer Fee

Arizona normally requires an Affidavit of Property Value, signed by both parties, to accompany any instrument transferring an interest in real property (ARS 11-1133). Gift deeds are specifically exempt from this requirement under ARS 11-1134(A)(7), and they are likewise exempt from the real estate transfer fee. The exemption still has to be claimed correctly on the face of the deed — a statement that the transfer is exempt, together with a citation to the specific exemption subsection, should appear below the legal description. A gift deed that omits the exemption recital is commonly rejected at the recorder's window as non-conforming, even though the transfer itself qualifies.

Federal Gift Tax

Arizona does not impose a state gift tax, but gifts of real property remain subject to federal gift tax under the Internal Revenue Code. The donor files the federal gift tax return (Form 709) when the value of the gift exceeds the annual exclusion amount, and the donor is primarily liable for any tax owed; if the donor does not pay, liability can shift to the donee. The donee does not treat the gift as income, but any rental or sale proceeds the donee receives after the transfer are taxable to the donee. The donee also takes the donor's carryover basis in the property rather than a stepped-up basis — an important planning difference between lifetime gifts and transfers at death. A CPA or estate planning attorney should review any gift involving significant value before the deed is executed.

Formatting, Recording, and Priority

Arizona's recording statute at ARS 11-480 imposes specific formatting requirements: legible type of at least ten points, white paper no larger than 8.5 by 14 inches, a caption identifying the document, and margins of at least two inches at the top of the first page (reserved for the recorder's stamp) and at least one-half inch elsewhere. County recorders reject non-conforming documents, and some counties enforce the margin rules strictly.

Record the deed in the county where the property is located, and confirm current fees and accepted forms of payment with the recorder's office in advance. Arizona is a race-notice jurisdiction under ARS 33-412: an unrecorded conveyance is void as against a subsequent purchaser for value who records first without notice of the prior transfer. Even gratuitous transfers benefit from prompt recording, because recording fixes the date of the gift for priority purposes and places the world on constructive notice of the donee's interest.

What's Included in the Download Package

The Arizona Gift Deed package includes the deed form, detailed guidelines covering the Arizona-specific drafting and recording requirements, and a completed example showing how the form should look for a typical family gift. All files are available for instant download after purchase.

How to Use This Form

- Select your county from the list above

- Download the county-specific form

- Fill in the required information

- Have the document notarized if required

- Record with your county recorder's office

What Others Like You Are Saying

"Love it"

"I had an issue due to the fact that I had many beneficiaries. I was and still am not sure how to han…"

"Appreciated the prompt answers to my inquiries…"

"So quick and easy"

"Very responsive and helpful. Made a big task quite easy and effecient. I would highly recommend. Rea…"

Compare with related Arizona forms

Important: County-Specific Forms

Our gift deed forms are specifically formatted for each county in Arizona.

After selecting your county, you'll receive forms that meet all local recording requirements, ensuring your documents will be accepted without delays or rejection fees.