Florida Gift Deed

County Specific Legal Forms Validated as recently as July 22, 2026 by our Forms Development Team

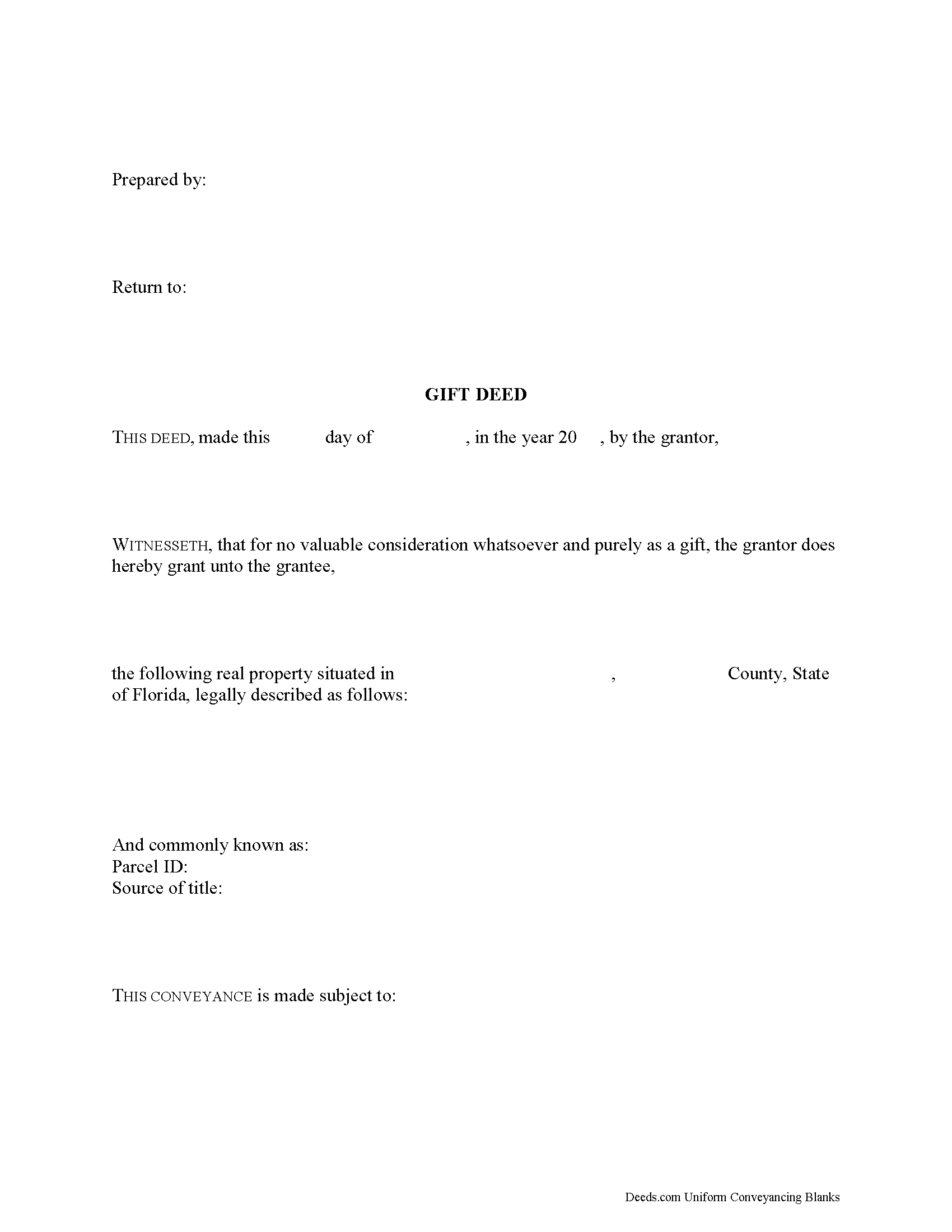

About the Florida Gift Deed

How to Use This Form

- Select your county from the list on the left

- Download the county-specific form

- Fill in the required information

- Have the document notarized if required

- Record with your county recorder's office

What Others Like You Are Saying

"Perfection. The filled-out form was especially helpful and I appreciate not having to share personal…"

"I was able to use your website for the purpose I was looking for. I was able to conclude the transac…"

"Fast and convenient."

"User friendly. Smooth transaction. I saved a lot of time"

"Thank you for making this so easy"

A Florida Gift Deed conveys real property without consideration, but the form has to clear several Florida-specific hurdles that catch many do-it-yourself transferors. Florida requires two subscribing witnesses on every deed in addition to a notary, the constitutional homestead protections force a non-titled spouse to join the deed when the property is the grantor's residence, and even a true gift with zero consideration is subject to documentary stamp tax — and to a much larger documentary stamp tax if the property carries a mortgage. A Florida-tailored gift deed addresses all of this on the face of the instrument so the clerk accepts it on first presentment.

When a Florida Gift Deed Is Commonly Used

Gift deeds are most often used for lifetime transfers between family members and for charitable conveyances — adding an adult child to title, transferring a vacation property to a sibling, conveying property between spouses (which Florida expressly authorizes by direct deed under Fla. Stat. 689.11), or donating raw land to a nonprofit. The defining feature of the gift deed is express language stating that no consideration is exchanged, which removes the conveyance from any warranty-pricing analysis and establishes donative intent for tax and probate purposes.

Florida Statutory Form Requirements

A Florida gift deed must include several elements that together satisfy the recording statutes:

- The grantor's full legal name and marital status — marital status is recited on Florida deeds because it determines whether spousal joinder is required for homestead

- The grantee's full legal name and post office address (Fla. Stat. 689.02)

- The property appraiser's parcel identification number, when available (Fla. Stat. 689.02)

- A complete legal description — for platted property, this typically references the lot, block, plat name, and the Plat Book and page number where the plat is recorded; condominium units reference the declaration recorded in the county Official Records

- The name and address of the person who prepared the deed (Fla. Stat. 695.26)

- Express language stating that the conveyance is made without consideration, which preserves the gift characterization

A source-of-title recital — referencing the deed under which the grantor took title — keeps the chain of title clean and lets a future title examiner trace ownership without ordering additional records.

Execution: Witnesses and Notary

Florida is one of the few states that still requires two subscribing witnesses on a deed conveying real property (Fla. Stat. 689.01). The notary may serve as one of the two witnesses, but a second, separate witness is still required. The grantor signs in the presence of all three — the two witnesses and the notary — and the notary then takes the acknowledgment in the form prescribed by Fla. Stat. 695.03. An out-of-state grantor may sign before a notary in their own state, but the acknowledgment must still substantially comply with the Florida form. Original wet-ink signatures are required; the clerk will reject photocopies.

Homestead and Spousal Joinder

This is the trap that voids more Florida gift deeds than any other. Article X, Section 4 of the Florida Constitution prohibits the owner of homestead from alienating the property without the joinder of the spouse — even when the spouse's name is not on the title. If a married grantor gifts homestead property and the spouse does not sign the deed, the conveyance is void as to the homestead. The same rule applies to gifts of homestead into the grantor's own revocable trust. Before signing a Florida gift deed, the grantor needs to determine whether the property is homestead and whether they are married — because if both answers are yes, the spouse joins the deed regardless of how title is held.

Documentary Stamp Tax on Gift Deeds

Florida imposes documentary stamp tax on deeds at the rate set by Fla. Stat. 201.02 — 70 cents per $100 of consideration (or fraction thereof) outside Miami-Dade County, with a different rate structure inside Miami-Dade. On a true gift with no consideration and no encumbrance, the minimum tax applies, calculated on the nominal consideration recited in the deed (typically $10 or "love and affection"). The trap is the mortgage: if the property being gifted is subject to an outstanding mortgage and the grantee takes title subject to that debt, the unpaid principal balance is treated as consideration and the documentary stamp tax is calculated on that balance. Grantors frequently discover this only when the clerk computes the tax at the recording counter. Confirming the documentary stamp tax with the clerk's office before recording prevents an unpleasant surprise.

Vesting Options for the Grantee

How title vests in the grantee should be stated on the face of the deed. Florida presumes that a conveyance to two or more grantees creates a tenancy in common unless the deed expressly says otherwise (Fla. Stat. 689.15). To create a joint tenancy with right of survivorship, the deed must include explicit survivorship language — a recital of "as joint tenants" alone is not sufficient. Married grantees may take title as tenants by the entirety, a Florida vesting form available only to spouses that carries automatic survivorship and significant creditor protection during the marriage. Tenancy by the entirety is generally presumed when real property is conveyed to a married couple, but the deed should still recite the marital status and the entireties vesting expressly to avoid ambiguity in the chain of title.

Recording the Deed

The executed gift deed is recorded in the Official Records of the county where the property is located. Florida is a race-notice jurisdiction under Fla. Stat. 695.01 — an unrecorded deed is good between the parties but is not protected against a subsequent good-faith purchaser who records first without notice. Prompt recording protects the grantee's title.

Recording-formatting rules under Fla. Stat. 695.26 apply at the clerk's window: the first page must include a three-inch top margin clear of text for the clerk's recording stamp, with one-inch margins elsewhere; the names of the grantor and grantee must be legibly printed below their signatures; and the prepared-by block must appear on the first page. Documentary stamp tax is collected at the time of recording. Some counties additionally require a recording cover sheet or a separate property appraiser's return — county-specific requirements should be confirmed with the clerk before submitting the deed.

Tax Considerations

Florida imposes no state gift tax. Federal gift tax may apply to the grantor — the IRS sets an annual exclusion per recipient that is adjusted for inflation, and gifts above that amount require the grantor to file Form 709. The grantee does not report the gift as income, but any income the property generates after the transfer is taxable to the new owner. The grantee also takes the grantor's basis in the property, which has consequences when the property is later sold. A tax professional should be consulted for any gift of significant value.

What's Included in the Florida Gift Deed Package

The Florida Gift Deed package available for download from Deeds.com includes:

- The Florida Gift Deed form, formatted to the recording-margin requirements of Fla. Stat. 695.26

- Step-by-step completion guidelines covering the homestead spousal-joinder analysis, vesting recitals, and the witness-and-notary execution sequence

- A completed sample showing how a typical Florida gift deed is filled in

The forms are provided in fillable Microsoft Word and PDF formats and are valid in every Florida county.

How to Use This Form

- Select your county from the list above

- Download the county-specific form

- Fill in the required information

- Have the document notarized if required

- Record with your county recorder's office

What Others Like You Are Saying

"Perfection. The filled-out form was especially helpful and I appreciate not having to share personal…"

"I was able to use your website for the purpose I was looking for. I was able to conclude the transac…"

"Fast and convenient."

"User friendly. Smooth transaction. I saved a lot of time"

"Thank you for making this so easy"

Compare with related Florida forms

Important: County-Specific Forms

Our gift deed forms are specifically formatted for each county in Florida.

After selecting your county, you'll receive forms that meet all local recording requirements, ensuring your documents will be accepted without delays or rejection fees.