Wyoming Interspousal Transfer Grant Deed

County Specific Legal Forms Validated as recently as July 17, 2026 by our Forms Development Team

About the Wyoming Interspousal Transfer Grant Deed

How to Use This Form

- Select your county from the list on the left

- Download the county-specific form

- Fill in the required information

- Have the document notarized if required

- Record with your county recorder's office

What Others Like You Are Saying

"Customer service was poor. I felt like I had to debate the representative to provide guidance and as…"

"EASY, PAINLESS, LOVED THE USER FRIENDLY INSTRUCTIONS"

"Process was simple, with a reasonable fee and within the suggested timetable for recordation. I high…"

"User friendly an FAST to access and use! Highly recommended."

"Wonderful service, very user friendly!"

Transferring Real Property between Spouses in Wyoming

In Wyoming, spouses have options for voluntary transfers of title to real property from one to the other. Quitclaim deeds can serve that purpose without specific guarantees, but an interspousal transfer grant deed offers more protection. In addition, using this type of deed avoids the necessity for property tax reassessment. They can also be used in situations where both spouses hold title to real estate and one transfers his or her interest in the property to the other. It can also be used in situations where one spouse holds title to real estate in sole ownership and voluntarily transfers his or her interest in the property to his or her spouse [1].

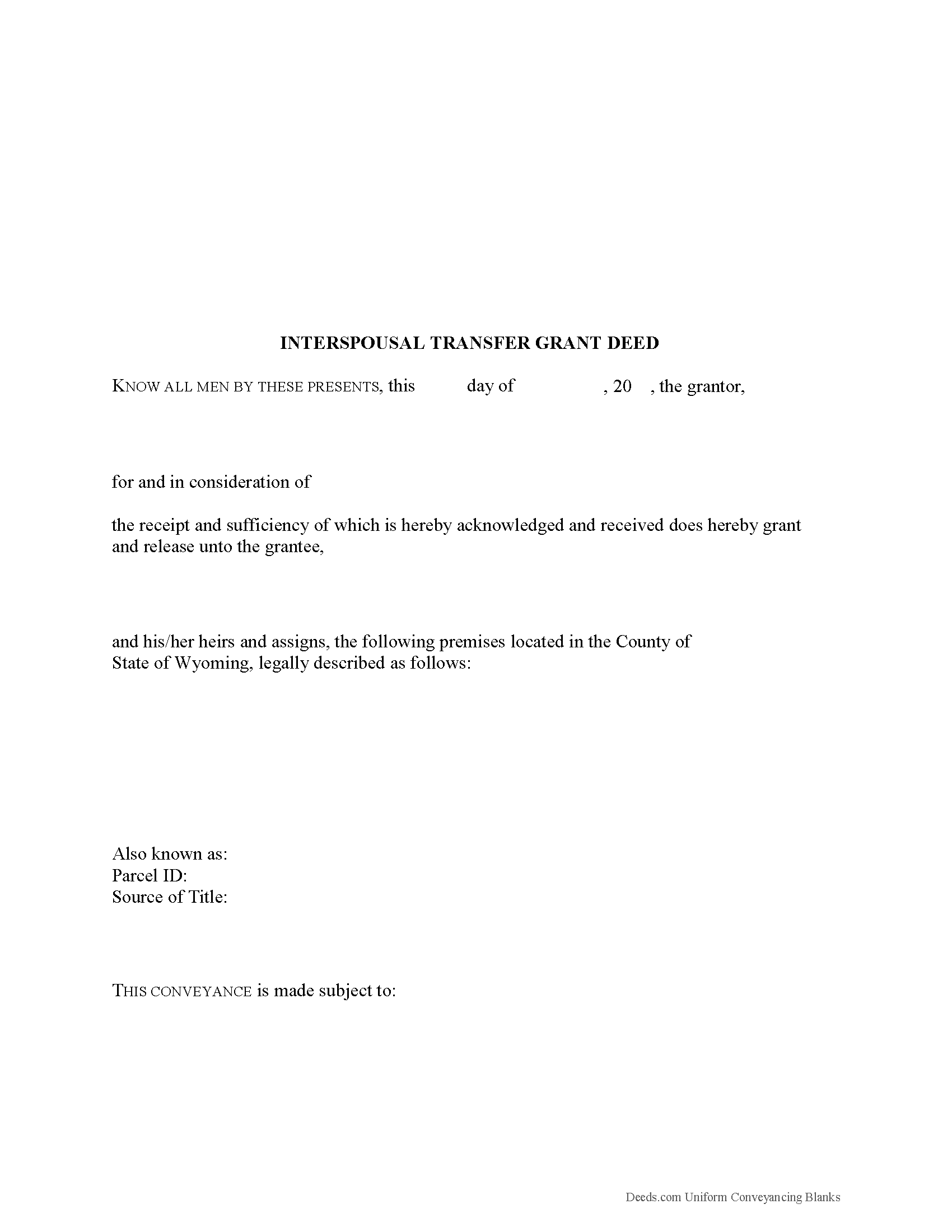

Unlike a quitclaim deed, a grant deed guarantees that the grantor (seller) has a present interest in the property, and, when recorded, provides evidence of a change of title to the grantee (buyer). It also includes a warranty that the property is not encumbered by any undisclosed liens or restrictions, which means that there are no legal claims to the title by third parties.

A lawful grant deed includes the grantor's full name, mailing address, and marital status, the consideration given for the transfer, and the grantee's full name, marital status, vesting, and mailing address. Vesting describes how the grantee holds title to the property. Generally, real property is owned in either sole ownership or in co-ownership. For Wyoming residential property, the primary methods for holding title are tenancy in common, joint tenancy, and tenancy by entirety. A conveyance of real estate to two unmarried persons creates a tenancy in common, unless another intention is clearly specified (Wyo. Stat. Ann. 34-1-140). Tenancy by entirety is only available to married couples, and is the presumed vesting unless otherwise stated.

As with any conveyance of realty, a grant deed requires a complete legal description of the parcel. Recite the prior deed reference to maintain a clear chain of title, and detail any restrictions associated with the property. Guarantees and responsibilities must be stated in the deed as well. These guarantees indicate that the grantor owns the property free and clear of encumbrances, and the seller assumes the responsibility for settling any future claims. If there is a time limit on the guarantees, it must also be incorporated in the deed. The finished copy of the deed must be duly signed by the parties and notarized. Record the original completed deed, along with any additional materials, with the clerk's office of the county where the property is located. Contact the same office to verify accepted forms of payment.

All Wyoming conveyances require a completed Statement of Consideration. Find this form on the county clerk's website, or through the Wyoming State Board of Equalization website. It is the responsibility of the buyer (or the buyer's agent) to fully complete the Statement of Consideration (Wyo. Stat. Ann 34-1-142) and to pay any applicable transfer taxes.

In some cases, there is no exchange of consideration when the property is transferred using an interspousal transfer grant deed. The federal government may identify such transfers as gifts, and which are potentially subject to the federal gift tax. The transfer of property from a spouse or former spouse isn't subject to gift tax if it meets any of the following exceptions: It is made in settlement of marital support rights, it qualifies for the marital deduction, it is made under a divorce decree, or it is made under a written agreement, and the couple is divorced within a specified period. If the transfer of property doesn't qualify for an exemption, or only qualifies in part, report that the transfer is subject to gift tax on IRS Form 709 [2], [3].

This article is provided for informational purposes only and is not a substitute for the advice of an attorney. Contact a Wyoming lawyer with any questions about interspousal transfers or other matters related to the transfer of real property.

[1] https://www.boe.ca.gov/proptaxes/pdf/ah401.pdf

[2] https://www.irs.gov/businesses/small-businesses-self-employed/frequently-asked-questions-on-gift-taxes

(Wyoming ITGD Package includes form, guidelines, and completed example)

How to Use This Form

- Select your county from the list above

- Download the county-specific form

- Fill in the required information

- Have the document notarized if required

- Record with your county recorder's office

What Others Like You Are Saying

"Customer service was poor. I felt like I had to debate the representative to provide guidance and as…"

"EASY, PAINLESS, LOVED THE USER FRIENDLY INSTRUCTIONS"

"Process was simple, with a reasonable fee and within the suggested timetable for recordation. I high…"

"User friendly an FAST to access and use! Highly recommended."

"Wonderful service, very user friendly!"

Other versions of this form

Compare with related Wyoming forms

Important: County-Specific Forms

Our interspousal transfer grant deed forms are specifically formatted for each county in Wyoming.

After selecting your county, you'll receive forms that meet all local recording requirements, ensuring your documents will be accepted without delays or rejection fees.