Massachusetts Estate Tax Affidavit

County Specific Legal Forms Validated as recently as July 21, 2026 by our Forms Development Team

About the Massachusetts Estate Tax Affidavit

How to Use This Form

- Select your county from the list on the left

- Download the county-specific form

- Fill in the required information

- Have the document notarized if required

- Record with your county recorder's office

What Others Like You Are Saying

"The site was easy to navigate."

"The process for obtaining document itself was easy, and the included guide and example are great! I …"

"Excellent service, communication and done in a timely fashion. Worth the cost for the convenience an…"

"Had pretty much everything I needed. Had to slice and dice a bit."

"had exactly what i needed and good price"

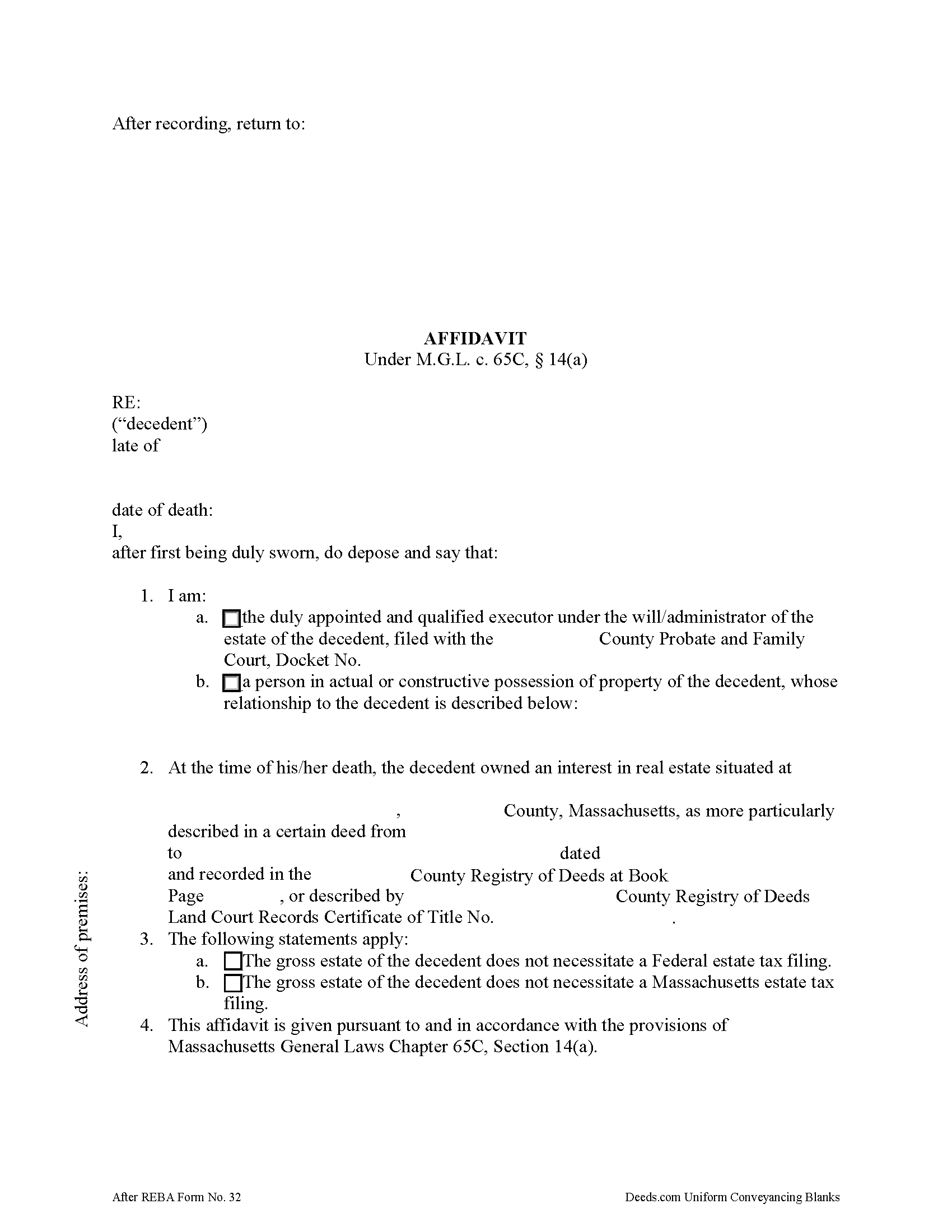

In Massachusetts, upon death, a lien attaches to a decedent's real property for ten years, or until the estate tax is paid, or an affidavit showing that the decedent's gross estate does not require an estate tax filing is recorded by a personal representative (or other qualified person under G. L. c. 65C, 6(a)) in the Registry of Deeds.

Use the affidavit of estate tax under M.G.L. c. 65C, 14(a) to release the lien on the decedent's property. The affidavit should include the name, address, and date of death of the decedent. The affiant shall indicate whether he/she is the personal representative of the decedent's probated estate, or, if the property is not subject to probate, then the affiant's relationship to the decedent.

The document's recitals also include the address of the premises affected and the prior instrument containing a legal description of the property. All statements contained within the affidavit are made by the affiant on penalty of perjury and sworn to before a notary public.

Contact a lawyer with questions about the Massachusetts estate tax and affidavits relating to decedents' estates in the Commonwealth of Massachusetts.

(Massachusetts ETA Package includes form, guidelines, and completed example)

How to Use This Form

- Select your county from the list above

- Download the county-specific form

- Fill in the required information

- Have the document notarized if required

- Record with your county recorder's office

What Others Like You Are Saying

"The site was easy to navigate."

"The process for obtaining document itself was easy, and the included guide and example are great! I …"

"Excellent service, communication and done in a timely fashion. Worth the cost for the convenience an…"

"Had pretty much everything I needed. Had to slice and dice a bit."

"had exactly what i needed and good price"

Compare with related Massachusetts forms

Important: County-Specific Forms

Our estate tax affidavit forms are specifically formatted for each county in Massachusetts.

After selecting your county, you'll receive forms that meet all local recording requirements, ensuring your documents will be accepted without delays or rejection fees.