Wisconsin Transfer on Death Deed

County Specific Legal Forms Validated as recently as July 14, 2026 by our Forms Development Team

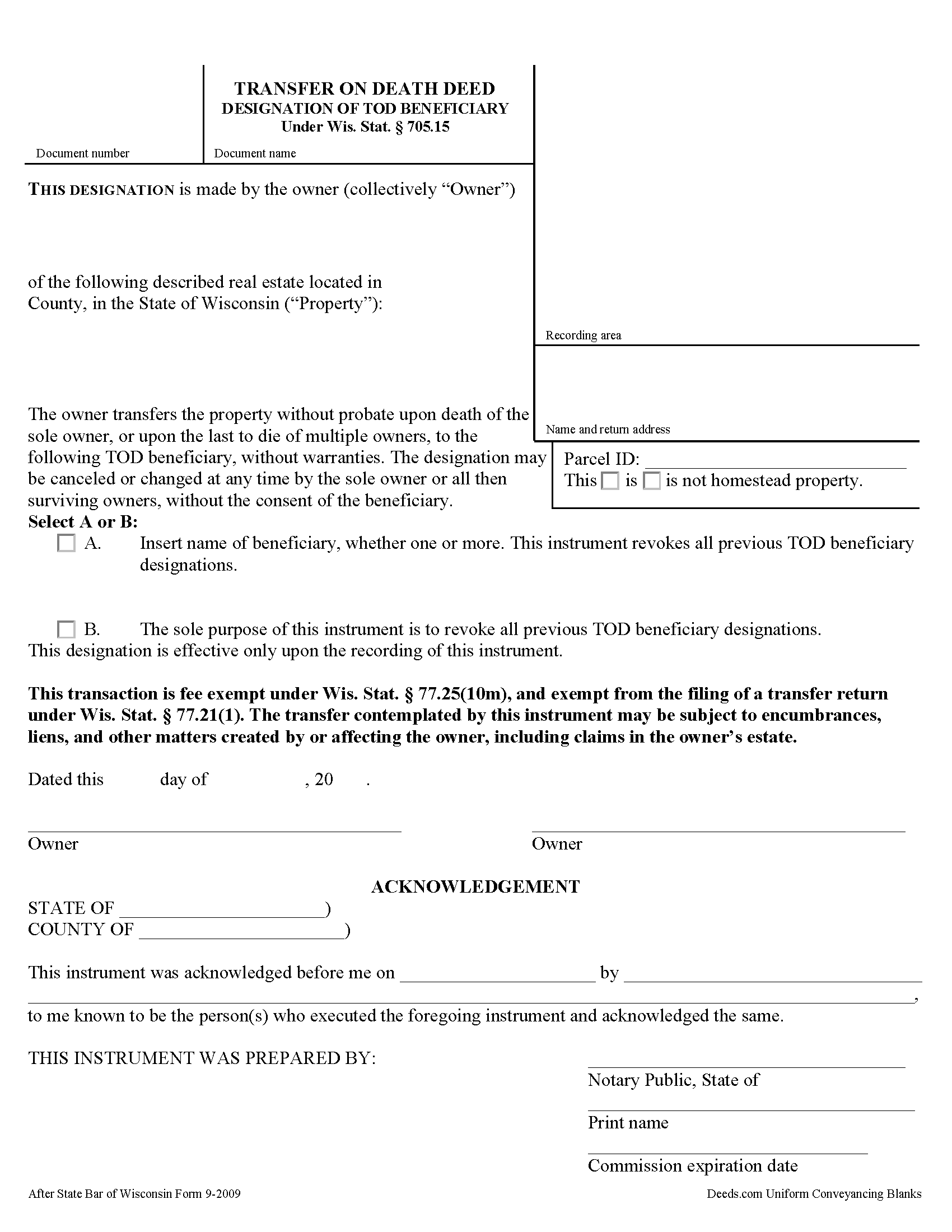

About the Wisconsin Transfer on Death Deed

How to Use This Form

- Select your county from the list on the left

- Download the county-specific form

- Fill in the required information

- Have the document notarized if required

- Record with your county recorder's office

What Others Like You Are Saying

"so far so good. thanks"

"High rating, great site and forms were exactly what I needed. Thanks for being there for me."

"Absolutely awesome! Quick, easy and efficient. I will definitely be using again!"

"Great forms, easy to use if you have at least a sixth grade education."

"Worked out good can the forms be filled out on the computer and printed off."

Under Wisconsin Statutes section 705.15, owners of real property in Wisconsin may designate one or more people to gain ownership of their property outside of the probate process. The transfer on death deed form contains the designation and must be recorded, DURING THE OWNER'S NATURAL LIFE, for validity.

By executing and recording a transfer on death beneficiary designation, the owner retains absolute control over the real estate, and may sell, mortgage, or use the property in any legal manner, and change or revoke the beneficiary designation without penalty or obligation to inform the beneficiary.

Because the transfer does not occur until after the owner's death, there is no transfer tax due when recording the deed under 77.21(1) and 77.25(10m). While the change in ownership happens as a function of law when the owner dies, when the beneficiary claims the land, he or she must record form TOD-110 to make the transfer official and enter the updated information into the public records.

Wisconsin's transfer on death deeds are useful estate planning tools. Even so, carefully consider the potential impact of a non-probate transfer of property on taxes, as well as eligibility for local, state, and federal benefits. Each case is unique, so contact an attorney with questions or for complex situations.

(Wisconsin TODD Package includes form, guidelines, and completed example)

How to Use This Form

- Select your county from the list above

- Download the county-specific form

- Fill in the required information

- Have the document notarized if required

- Record with your county recorder's office

What Others Like You Are Saying

"so far so good. thanks"

"High rating, great site and forms were exactly what I needed. Thanks for being there for me."

"Absolutely awesome! Quick, easy and efficient. I will definitely be using again!"

"Great forms, easy to use if you have at least a sixth grade education."

"Worked out good can the forms be filled out on the computer and printed off."

Other versions of this form

Compare with related Wisconsin forms

Important: County-Specific Forms

Our transfer on death deed forms are specifically formatted for each county in Wisconsin.

After selecting your county, you'll receive forms that meet all local recording requirements, ensuring your documents will be accepted without delays or rejection fees.