Coconino County Deed of Trust Form

Last validated July 28, 2026 by our Forms Development Team

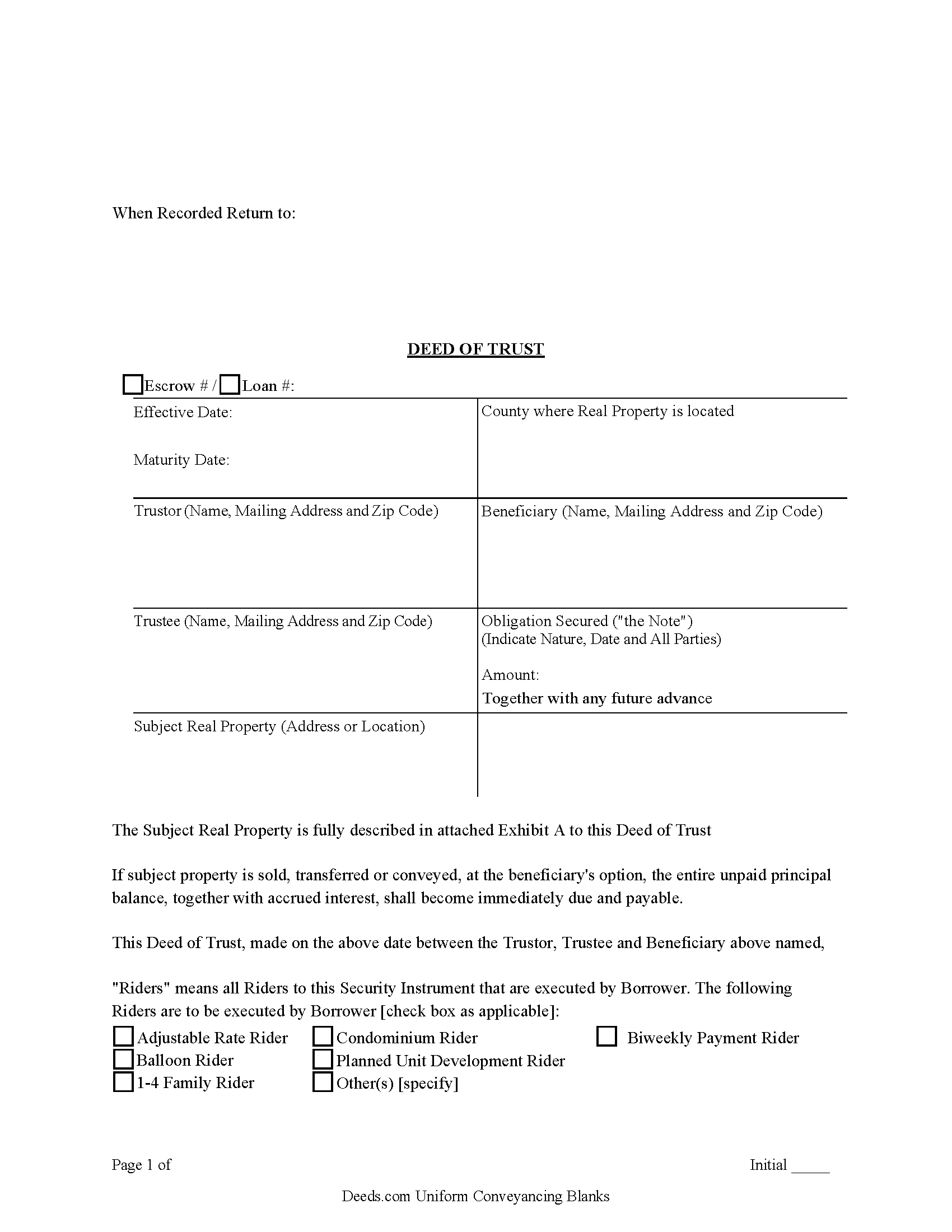

Coconino County Deed of Trust Form

Fill in the blank form formatted to comply with all recording and content requirements.

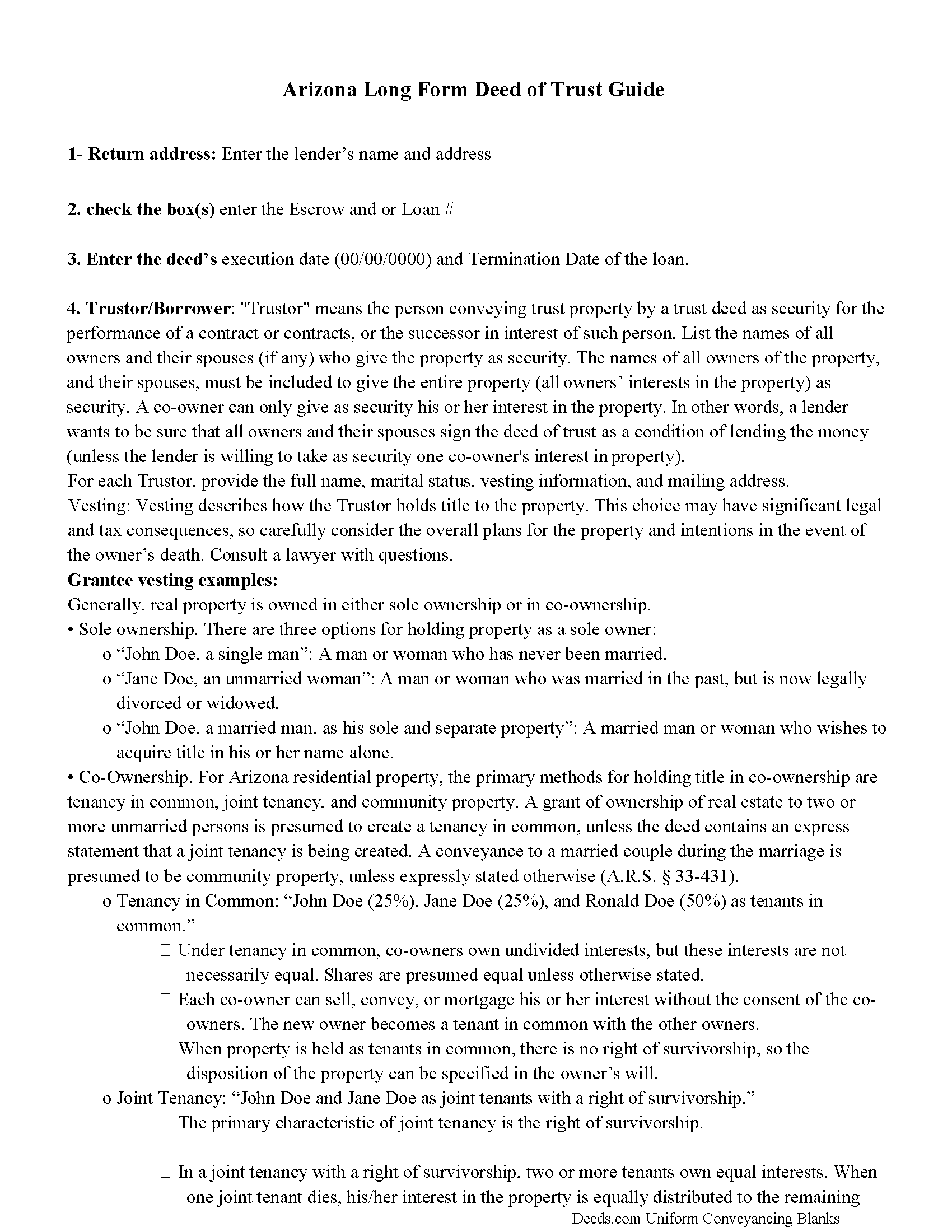

Coconino County Deed of Trust Guidelines

Line by line guide explaining every blank on the form.

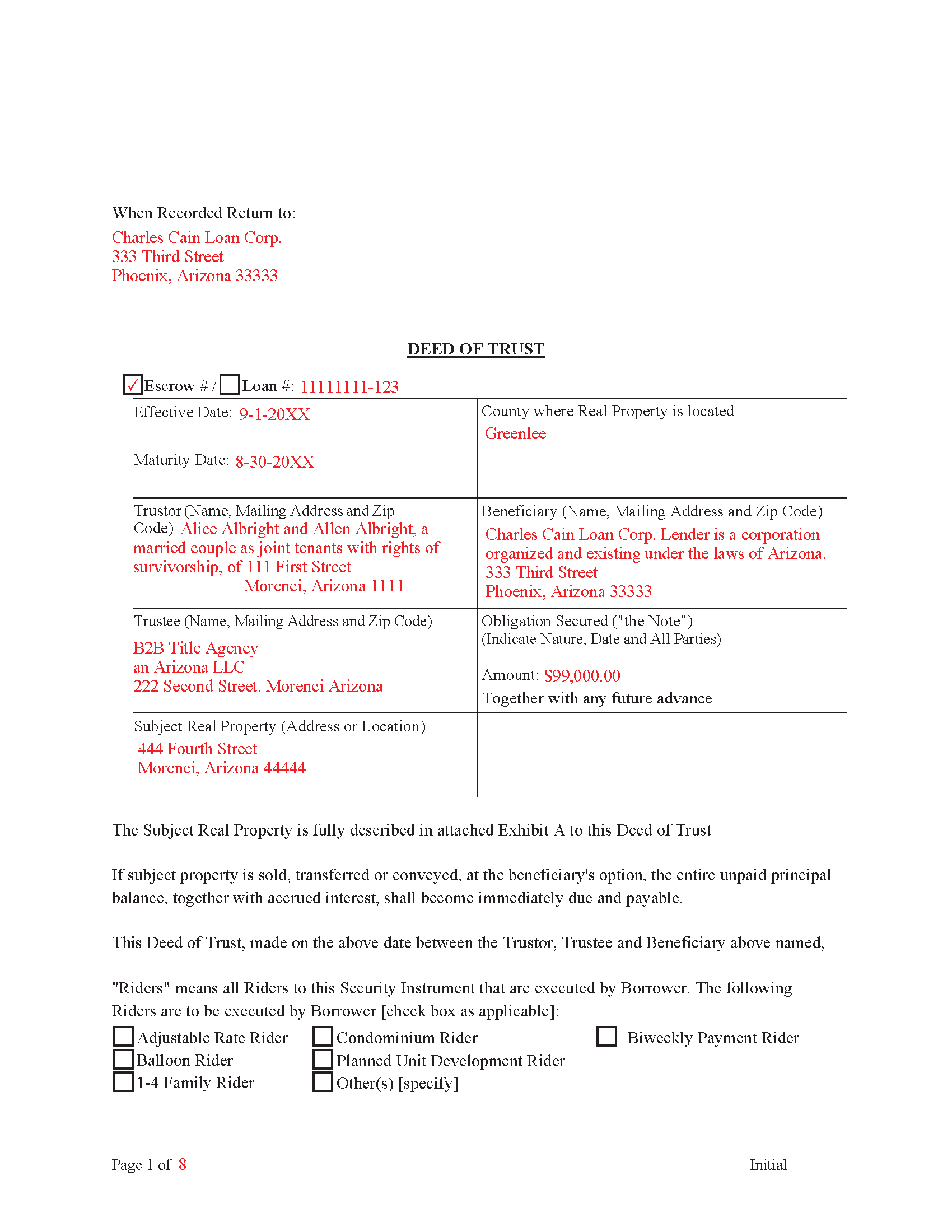

Coconino County Completed Example of the Deed of Trust

Example of a properly completed form for reference.

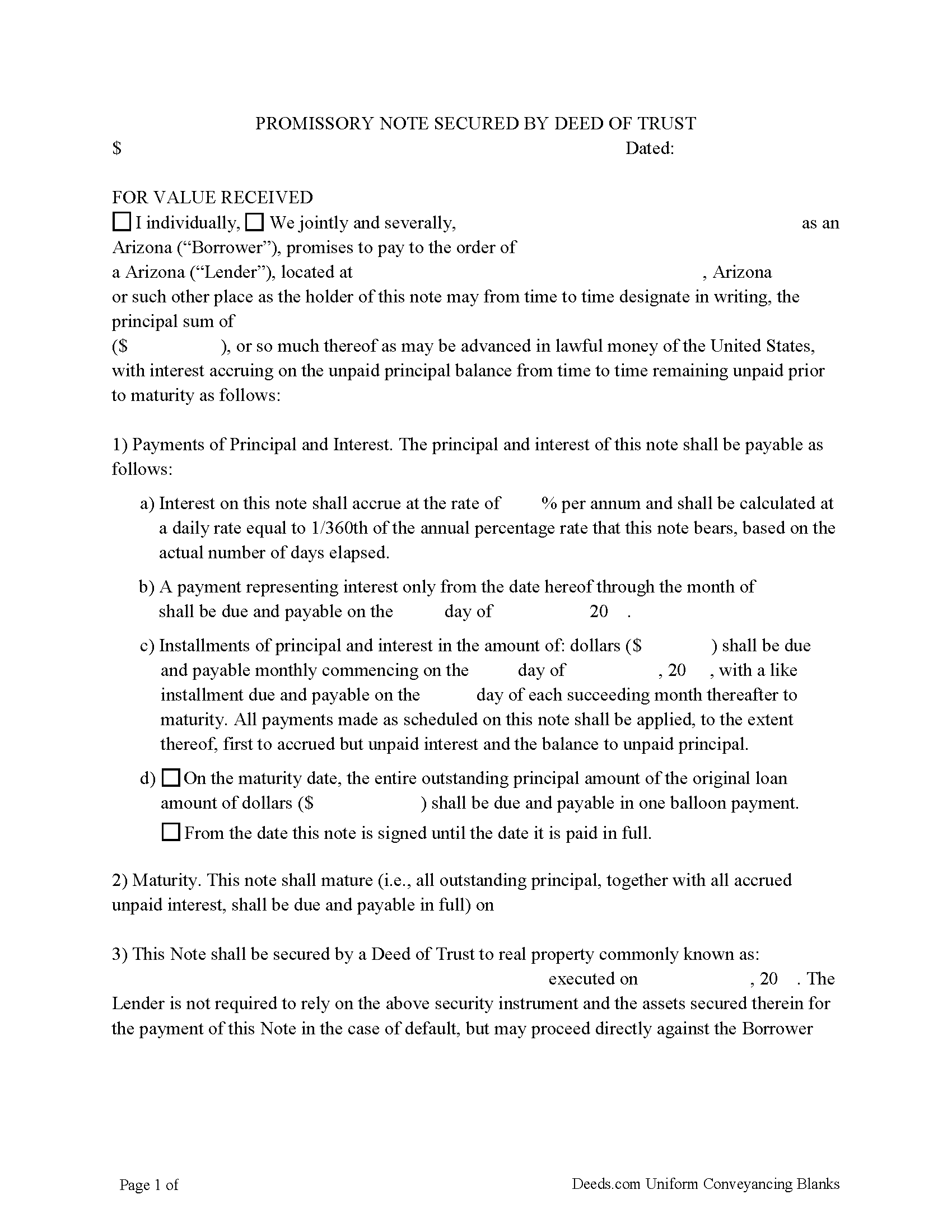

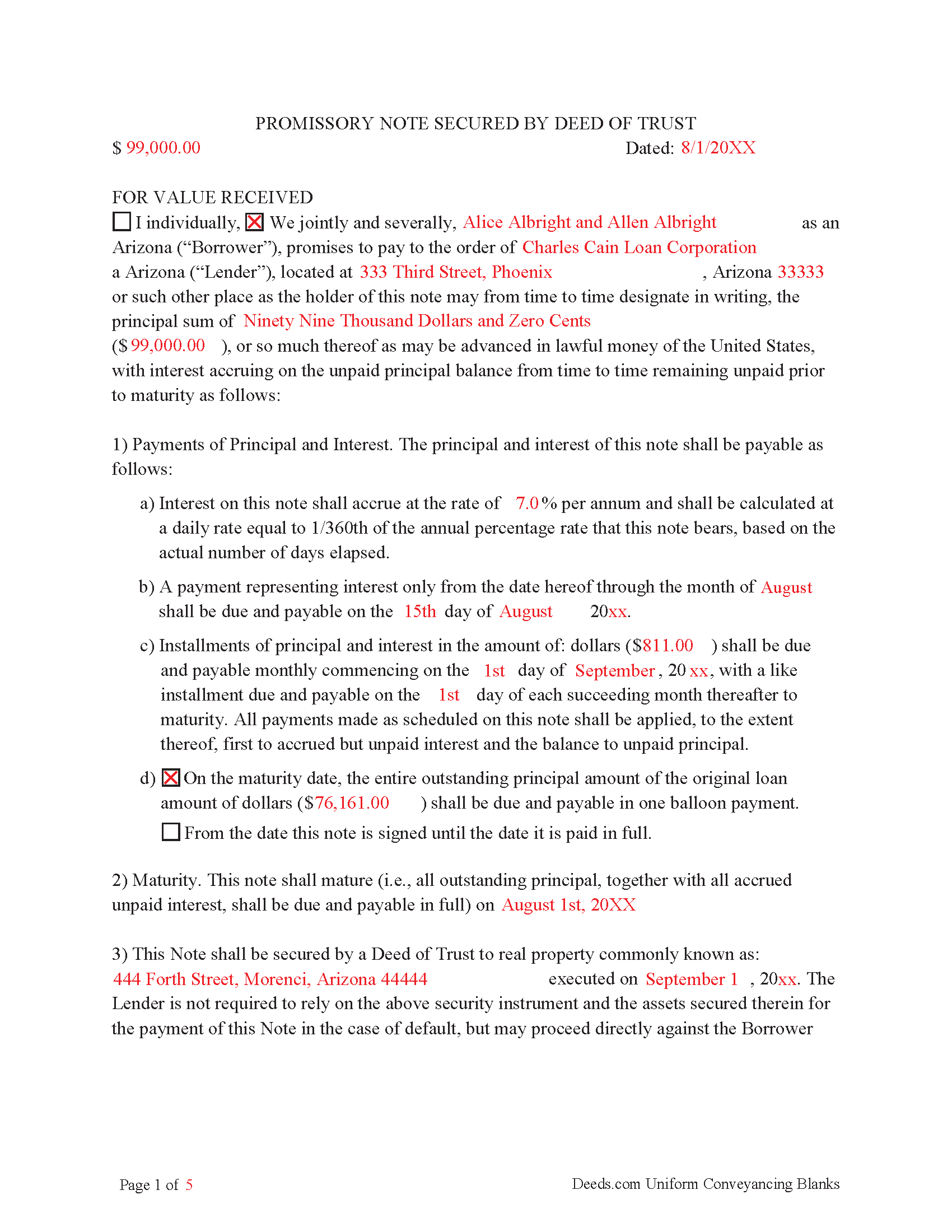

Coconino County Promissory Note Form

Note that is secured by the Deed of Trust. Can be used for traditional installments or balloon payment.

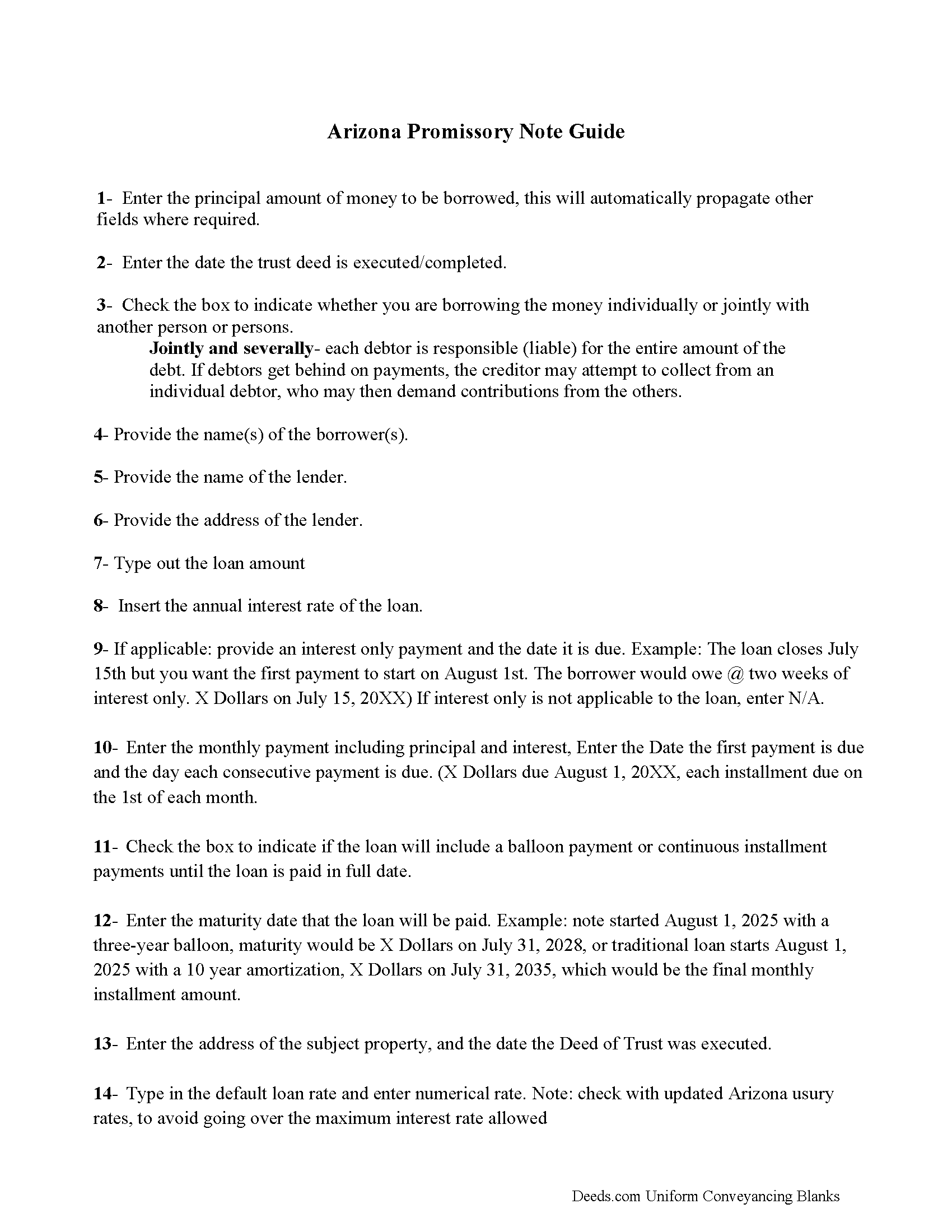

Coconino County Promissory Note Guidelines

Line by line guide explaining every blank on the form.

Coconino County Completed Example of the Promissory Note

This Arizona Promissory Note is filled in and highlighted, showing how the guideline information, can be interpreted into the document.

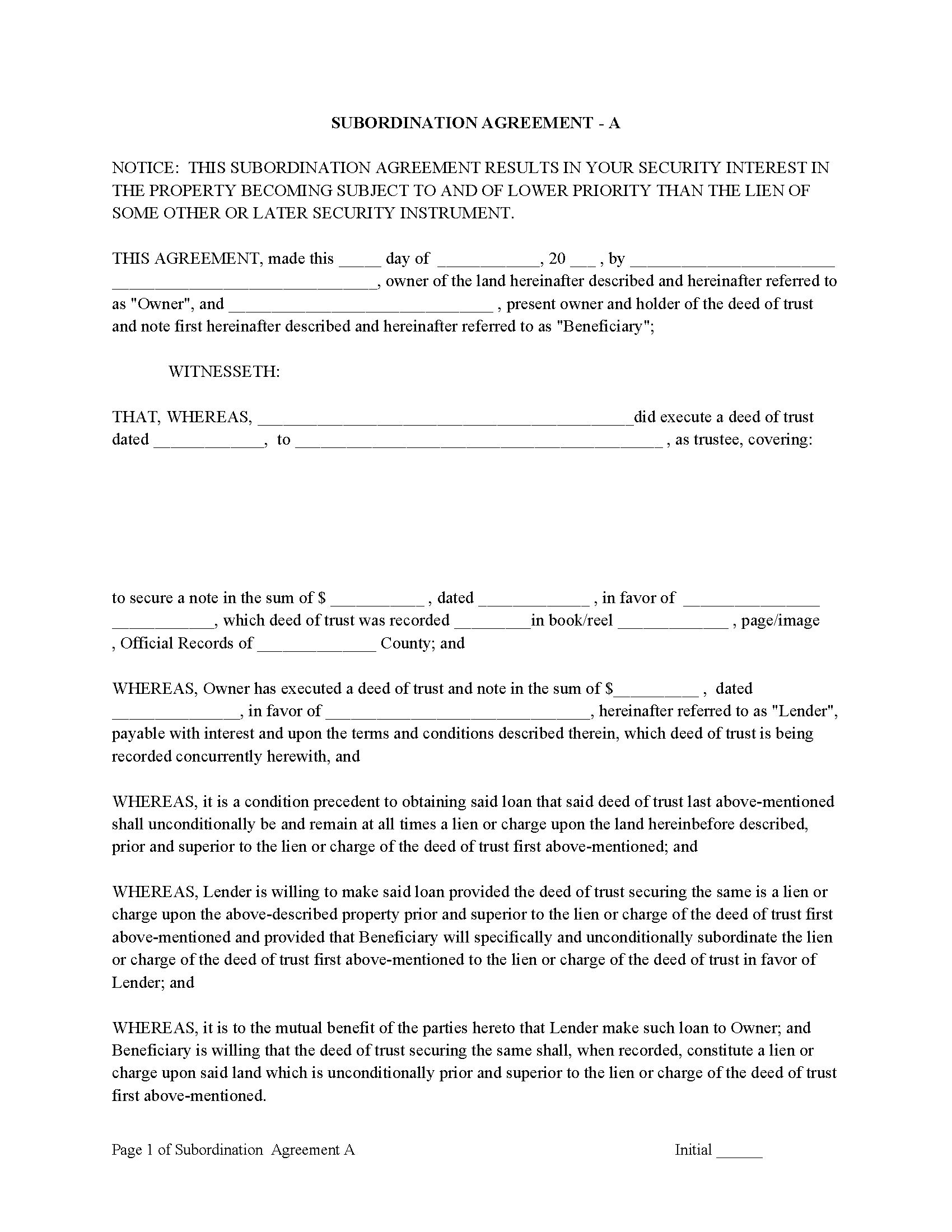

Coconino County Subordination Clauses

Used to place priority on claim of debt. Included are 4 clauses for unique situations. If needed, add to D.O.T. as an addendum or rider.

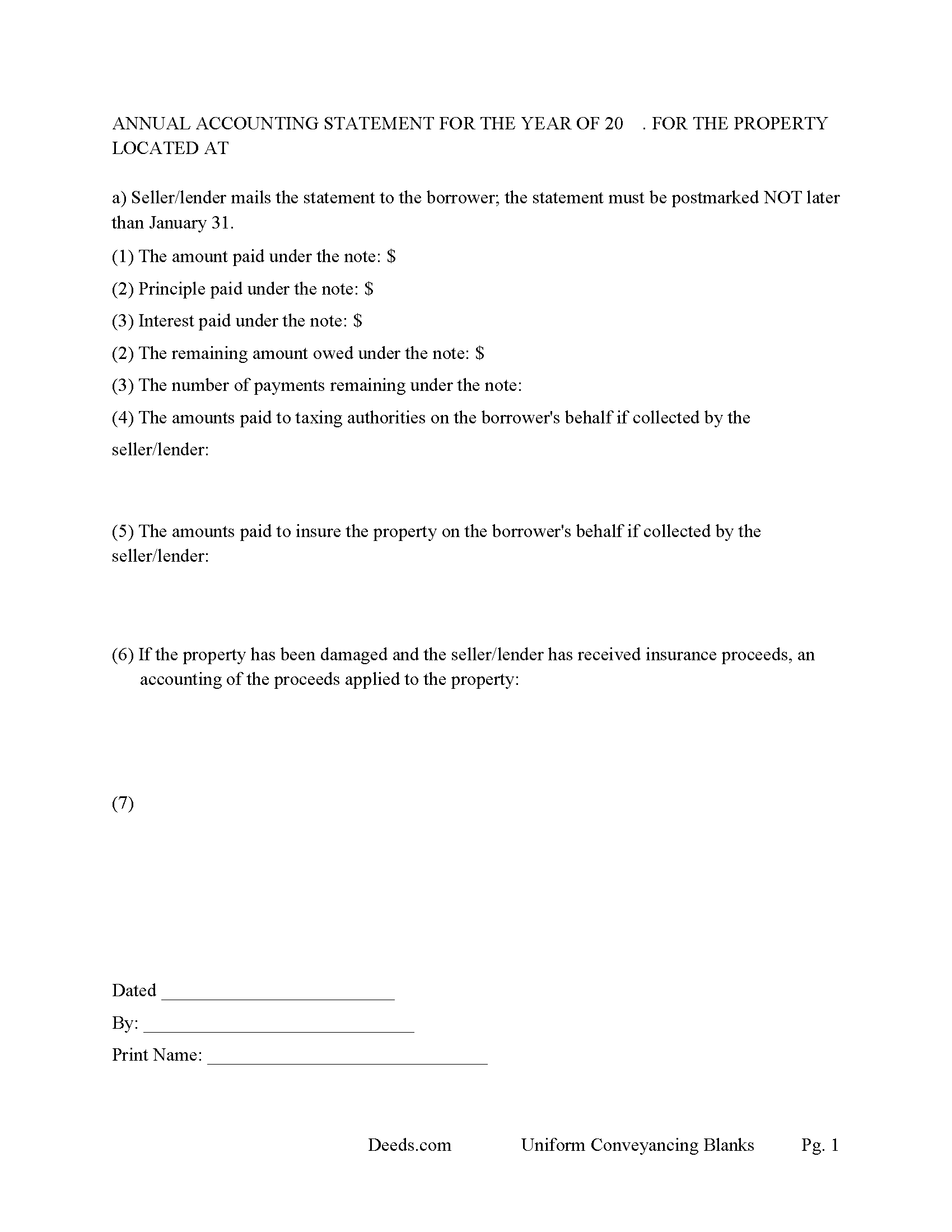

Coconino County Annual Accounting Statement

Mail to borrower for fiscal year reporting.

All 8 documents above included • One-time purchase • No recurring fees

Immediate Download • Secure Checkout

Additional Arizona and Coconino County documents included at no extra charge:

Where to Record Your Documents

County Recorder Office

Flagstaff, Arizona 86001

Hours: 8:00am to 5:00pm Monday - Friday

Phone: 928-679-7850 or 800-793-6181

Recording Tips for Coconino County:

- White-out or correction fluid may cause rejection

- Ask about their eRecording option for future transactions

- Bring extra funds - fees can vary by document type and page count

- Have the property address and parcel number ready

- Recording early in the week helps ensure same-week processing

Cities and Jurisdictions in Coconino County

Properties in any of these areas use Coconino County forms:

- Bellemont

- Cameron

- Flagstaff

- Forest Lakes

- Fredonia

- Grand Canyon

- Gray Mountain

- Happy Jack

- Kaibeto

- Leupp

- Marble Canyon

- Mormon Lake

- Munds Park

- North Rim

- Page

- Parks

- Sedona

- Supai

- Tonalea

- Tuba City

- Williams

Hours, fees, requirements, and more for Coconino County

How do I get my forms?

Forms are available for immediate download after payment. The Coconino County forms will be in your account ready to download to your computer. An account is created for you during checkout if you don't have one. Forms are NOT emailed.

Are these forms guaranteed to be recordable in Coconino County?

Yes. Our form blanks are guaranteed to meet or exceed the applicable formatting requirements used for recording in Coconino County, including margin requirements, font requirements, and other layout standards. This guarantee applies to formatting, not to the legal sufficiency of information entered by the user or the suitability of a form for a particular transaction.

Can I reuse these forms?

Yes. You can reuse the forms for your personal use. For example, if you have multiple properties in Coconino County you only need to order once.

What do I need to use these forms?

The forms are PDFs that you fill out on your computer. You'll need Adobe Reader (free software that most computers already have). You do NOT enter your property information online - you download the blank forms and complete them privately on your own computer.

Are there any recurring fees?

No. This is a one-time purchase. Nothing to cancel, no memberships, no recurring fees.

How much does it cost to record in Coconino County?

Recording fees in Coconino County vary. Contact the recorder's office at 928-679-7850 or 800-793-6181 for current fees.

Questions answered? Let's get started!

The Arizona Deed of Trust is the dominant security instrument for loans against Arizona real property, used in place of the traditional mortgage because it permits non-judicial foreclosure through a trustee's sale under ARS 33-807 — materially faster and less expensive than judicial foreclosure of a mortgage. The structure requires three parties rather than two: the trustor (the borrower), the beneficiary (the lender), and a trustee (a neutral third party authorized under ARS 33-803 to hold bare legal title to the property and conduct any required sale on default). That three-party structure is not cosmetic. It is what enables the non-judicial foreclosure remedy that makes the deed of trust preferred over a mortgage in Arizona, and it imposes statutory qualification requirements on who can serve as trustee that do not exist for lenders or borrowers.

When the Arizona Deed of Trust Is Used

Deeds of trust are used to secure virtually every meaningful loan against Arizona real property. Typical uses include institutional residential mortgages, commercial real estate loans, construction loans, home equity lines of credit, seller-financed transactions where the buyer gives back a purchase-money deed of trust to secure a promissory note to the seller, hard money loans from private investors, and loans between related entities in complex ownership structures. The form works for owner-occupied residential property, investment properties, condominiums, rental property (with a rider addressing rental use), and commercial parcels. The stringent default terms and strict covenants that make the form well-suited to investor and seller-financed transactions also make it appropriate for institutional lending, where the lender is typically unwilling to compromise on default remedies in exchange for the attractiveness of Arizona's foreclosure process.

Why a Deed of Trust Rather Than a Mortgage

Arizona law recognizes both mortgages and deeds of trust, but they foreclose differently. A mortgage must be foreclosed judicially under ARS 33-721 et seq., which means filing a lawsuit, obtaining a judgment, and conducting a sheriff's sale — a process that typically takes many months and generates substantial legal expense. A deed of trust can be foreclosed non-judicially through a trustee's sale under ARS 33-807, with statutory notice periods and a public auction conducted by the trustee, typically completed in about four months from the recording of the notice of trustee's sale. The non-judicial process avoids court involvement entirely when no one contests it, and the statutory framework gives both borrowers and lenders predictable timelines and procedures. Lenders prefer the faster remedy; borrowers benefit from the clear, statutory cure periods; the Arizona real estate market has priced the difference into its expectations. The result is that mortgages are comparatively rare in current Arizona practice, and the deed of trust is the working instrument for almost all secured real estate lending.

The Trustee's Role

The trustee is not the lender and not a mere formality. Under ARS 33-803, only qualified persons may serve as trustee: active Arizona-licensed attorneys and Arizona-licensed escrow agents are the most common in current practice, along with certain banks, savings institutions, title insurance companies doing business in Arizona, and licensed real estate brokers acting as escrow agents. The trustee holds bare legal title to the property on behalf of the beneficiary and, if default occurs, conducts the trustee's sale under the statutory framework. The trustee is required to act impartially — not as an advocate for the lender, not as an advocate for the borrower. Selection of a qualified trustee is not optional: a deed of trust naming an unqualified party as trustee creates problems when foreclosure is actually needed. Most Arizona deeds of trust name a trustee at the time of recording and allow the beneficiary to substitute a successor trustee under ARS 33-804 if the named trustee becomes unavailable or unwilling to act.

Anti-Deficiency Protection

Arizona's anti-deficiency statute at ARS 33-814 is one of the most significant consumer protections in any state's real estate law and must be understood by every party to a deed of trust. After a trustee's sale on a deed of trust securing a purchase-money loan for residential property of 2.5 acres or less, used as a single one-family or two-family dwelling, the beneficiary generally cannot pursue the borrower for any deficiency — the sale is the lender's sole remedy. This protection transforms the economic calculus of Arizona residential lending: a borrower in distress on a qualifying purchase-money loan faces loss of the property but not personal liability for the shortfall. Lenders have adjusted underwriting accordingly, and the state's housing market operates against this legal backdrop.

The anti-deficiency protection does not reach every deed of trust. Commercial properties, residential parcels larger than 2.5 acres, and non-purchase-money loans (refinances for other purposes, home equity loans taken out after purchase) fall outside the protection, and the beneficiary can pursue a deficiency judgment on those loans after a trustee's sale, subject to the fair value hearing framework under ARS 33-814. The interaction between loan purpose, property type, and post-sale liability is one of the most consequential and sometimes misunderstood areas of Arizona real estate finance, and borrowers considering a deed of trust should understand how the anti-deficiency rules apply to the specific loan being signed.

The Trustee's Sale Process

The non-judicial foreclosure process begins with the beneficiary instructing the trustee to record a Notice of Trustee's Sale in the county where the property is located. ARS 33-807 sets a statutory minimum period of ninety days from recording of the notice to the date of the sale, during which the trustee must publish notice in a newspaper of general circulation and mail or deliver notice to the trustor and other entitled parties under ARS 33-809. The trustor's right to reinstate the loan by curing the default exists during most of the pre-sale period under ARS 33-813 and generally ends at 5:00 p.m. on the day before the scheduled sale. Reinstatement requires payment of the defaulted amount, trustee's fees, and statutory costs — not the entire accelerated loan balance — which is a meaningful Arizona-specific protection for borrowers in temporary distress.

The sale itself is a public auction conducted by the trustee at a location specified in the notice, typically the courthouse of the county where the property is located. The property is sold to the highest bidder for cash or credit bid (in the case of the beneficiary). The trustee then issues a trustee's deed to the successful bidder, which conveys title free of subordinate liens and encumbrances. The trustee's deed is effective immediately upon recording; Arizona does not provide a statutory post-sale redemption period for trustee's sales, which distinguishes the non-judicial remedy from judicial foreclosure of a mortgage (where the borrower does have a statutory redemption period). This absence of post-sale redemption is another reason the deed of trust is the preferred security instrument.

Due-on-Sale and Transfer Restrictions

The deed of trust prohibits sale, conveyance, or further encumbrance of the property without the beneficiary's prior written consent. Violation is an event of default that can trigger acceleration and foreclosure. Federal law under the Garn-St Germain Depository Institutions Act preempts enforcement of due-on-sale clauses in certain situations, particularly for transfers to a surviving spouse or child of the borrower, transfers into a revocable trust for estate planning purposes where the borrower remains a beneficiary, and several other categories. The federal exemptions can prevent acceleration in scenarios that otherwise appear to breach the due-on-sale clause, but the exemptions are narrow and fact-specific, and borrowers relying on them should confirm the specific transaction qualifies before proceeding.

Events of Default

The deed of trust defines events of default more broadly than the promissory note it secures. Monetary defaults — missing a scheduled payment on the note — are the most common triggers, but the deed of trust reaches further. Failure to perform any duty required by the instrument (including maintenance of the property in good repair, maintenance of required insurance, and payment of property taxes) constitutes default. Transfer or attempted transfer without the beneficiary's consent constitutes default. Voluntary or involuntary further encumbrance without consent constitutes default. Removal of property included in the security (fixtures, attached equipment) without consent constitutes default. Abandonment of the property constitutes default. Filing of bankruptcy by or against the trustor, or adjudication of insolvency, constitutes default. Lease or attempted lease of the property when the loan was made on the basis of owner-occupancy can constitute default unless the beneficiary has approved in writing or a rental-use rider has been attached.

These non-monetary events of default are what make the deed of trust a stronger instrument than the note alone. A borrower who is current on payments but has let the property fall into disrepair, failed to maintain insurance, or encumbered the property with a second lien without consent has given the beneficiary grounds to accelerate and foreclose. The severity of that remedy is why Arizona courts and beneficiaries generally apply these grounds reasonably in practice, particularly where cure is available — but they remain in the instrument and carry force when invoked.

Trustor's Maintenance and Inspection Obligations

The trustor is required to take reasonable care of the property and maintain it in good repair and condition as at the original date of the deed of trust, with ordinary depreciation excepted. This covenant runs for the life of the deed of trust and can be enforced by the beneficiary through default remedies if breached. The trustee and beneficiary have the right to enter the property at reasonable times on prior notice to the trustor to inspect for compliance — a right that is included in the deed of trust but limited in practice by Arizona landlord-tenant and privacy considerations when the property is owner-occupied. For investment properties, the inspection right is more actively used, and lease riders on rental properties typically coordinate the lender's inspection right with the tenants' possession.

ARS 33-806 Damages Remedy

Arizona statute provides that the trustee or beneficiary can take action against any person — not just the trustor — for damages in specified categories: physical abuse or destruction of the trust property, waste, and impairment of the security provided by the trust deed. This remedy is independent of foreclosure and can be pursued while the deed of trust remains in place. It is particularly useful against third parties whose conduct damages the property (a neighbor whose construction impairs the security, a tenant who causes deliberate damage) or against trustors who engage in waste short of outright default. The statutory damages claim supplements the lender's foreclosure remedies rather than replacing them.

The Promissory Note — A Separate Instrument

A deed of trust secures repayment of a debt, but the debt itself is evidenced by a separate instrument — the promissory note. The note and the deed of trust work together: the note creates the personal obligation to repay and sets the interest rate, payment schedule, maturity date, and other economic terms, while the deed of trust attaches that obligation to the real property as collateral. A loan transaction typically involves executing both documents at the same closing. The note is not usually recorded (it is a personal obligation, not a real property instrument), but the deed of trust must be recorded against the property to perfect the security interest. When the loan is paid in full, the beneficiary releases the deed of trust through a recorded release or substitution of trustee and release, and the note should be marked paid and returned to the borrower.

Subordination

In transactions involving multiple liens — construction loans and permanent financing, purchase-money deeds of trust and subsequent bank loans, private seller financing and institutional refinancing — the relative priority of the deeds of trust matters. Priority generally follows recording order under Arizona's race-notice rule at ARS 33-412, but parties can change that order by agreement through a subordination clause in the deed of trust or a separate subordination agreement. A senior lienholder who subordinates to a junior lienholder steps behind the junior in priority, which has significant consequences at foreclosure. Subordination clauses are common in seller-financed transactions where the seller's deed of trust is expected to remain in place while the buyer refinances with institutional lenders.

Execution and Recording

Under ARS 33-401, a deed of trust must be in writing, subscribed by the trustor, and acknowledged before a notary public or other officer authorized to take acknowledgments. Arizona does not require subscribing witnesses. Arizona is a community property state, and when the property is community property, both spouses must sign the deed of trust; a deed of trust executed by one spouse alone does not create an enforceable security interest in community property over the objection of the non-signing spouse. Recording is under ARS 33-411 and the priority rule at 33-412; the deed of trust should be recorded in the county where the property is located, promptly, to establish priority. ARS 11-480 formatting requirements apply: ten-point or larger legible type, white paper no larger than 8.5 by 14 inches, a caption identifying the document, a top margin of at least two inches on the first page reserved for the recorder's stamp, and half-inch minimums elsewhere.

Annual Accounting and Release on Payoff

Borrowers under Arizona deeds of trust are entitled to an annual accounting from the beneficiary showing payment history, interest charged, principal balance, and any escrow activity. The statement supports the borrower's ability to verify the loan's status and to detect errors, and it is particularly important in seller-financed transactions where the parties may not be running institutional loan-servicing systems. On payoff, the beneficiary is obligated to execute and deliver a release or substitution of trustee and release that can be recorded to clear the deed of trust from the chain of title. Failure to deliver a timely release after payoff creates a cloud the former borrower cannot easily remove without pursuing the beneficiary, and Arizona law provides remedies against beneficiaries who unreasonably delay.

What's Included in the Download Package

The Arizona Deed of Trust package includes the deed of trust form drafted around the ARS 33-801 et seq. framework with the trustee, beneficiary, and trustor structure required for non-judicial foreclosure, a separate promissory note form with its own guidelines and completed example that works in tandem with the deed of trust, subordination clause forms for transactions involving multiple liens, an annual accounting statement form for the beneficiary's use during the life of the loan, detailed guidelines covering the Arizona-specific drafting and recording requirements and the interaction between the security instrument and the note, and a completed example showing how the deed of trust should look for a typical transaction. The form is suitable for owner-occupied residential property, investor and rental property (with appropriate rider), condominiums, and commercial parcels. All files are available for instant download after purchase.

Important: Your property must be located in Coconino County to use these forms. Documents should be recorded at the office below.

This Deed of Trust meets all recording requirements specific to Coconino County.

Our Promise

The documents you receive here are guaranteed to meet or exceed the applicable Coconino County recording format requirements. If there is a rejection caused by our formatting, we will correct the issue or refund your payment. This guarantee applies to document formatting only and does not extend to information entered by the user, the selection of the form, or the legal effect of the completed document.

Save Time and Money

Get your Coconino County Deed of Trust form done right the first time with Deeds.com Uniform Conveyancing Blanks. At Deeds.com, we understand that your time and money are valuable resources, and we don't want you to face a penalty fee or rejection imposed by a county recorder for submitting nonstandard documents. We constantly review and update our forms to meet rapidly changing state and county recording requirements for roughly 3,500 counties and local jurisdictions.

4.8 out of 5 - ( 4763 Reviews )

Troy B.

July 8th, 2020

Very pleased with website very simple to navigate through

Thank you for your feedback. We really appreciate it. Have a great day!

Emili C.

October 14th, 2020

Thank you! I received my forms promptly and they are easy to follow along for filling out. The examples gave me confidence that they were done correctly.

Thank you for your feedback. We really appreciate it. Have a great day!

Rhonda E.

March 10th, 2021

Quick, easy, well-priced, and I have the forms that I need. PDFS download easily and are fillable! Thank you, Deeds.com!

Thank you!

Catherine E.

January 7th, 2021

I was referred to your company, but when i tried to process the recording of a deed to a property in City of Philadelphia my service was rejected. I appreciated the feedback i received from one of your representatives who instructed me in the right process for recording a deed in philadelphia. Thank you for all your help. The deed that needed to be recorded was overnighted yesterday. Stay safe and mask up

Thank you!

kelly W.

June 10th, 2019

Your customer service person was very professional and polite and helpful.

Thank you!

Dana G.

July 22nd, 2021

This service is WONDERUL. I spent 14 years trying to get a deed recorded properly. Deeds.com kept submitting and resubmitting after corrections until it was finally accepted. They did in one day what I couldn't get done in 14 years!

Thank you!

Josephine A.

June 9th, 2020

Being a first timer, I was hesitant at first to use the service. I was genuinely surprised at how easy it is to set up an account, upload my document, and pay the invoice. The next day I downloaded my document duly recorded. Good work, guys!

Thank you for your feedback. We really appreciate it. Have a great day!

Janet P.

July 30th, 2021

Extremely easy to use. The guide and sample were a great source of reference.

Thank you for your feedback. We really appreciate it. Have a great day!

Donald W.

December 8th, 2019

Could not have been any easier to download the quit claim forms. The provided instructions and samples look to be helpful. Only have to set aside the time to fill out. Thanks

Thank you!

Robert L.

September 28th, 2020

It was easy for me to open an account and upload a document for recording.

Thank you for your feedback. We really appreciate it. Have a great day!

JOHN F.

May 24th, 2023

Quick and easy! I had previously prepared a Lady Bird deed, submitted it through Deeds.com and it was accepted/recorded by my county in just a few hours. The Deed.com $21 fee was well worth it as I saved fuel, tolls and parking costs not to mention at least 2-3 hours of my time that it would've taken to get downtown and back home!

Thanks for the feedback John. We appreciate you taking the time to share your experience. Have an amazing day!

George Y.

June 24th, 2021

Thought it was great, no issues. Very convenient especially dealing with difficult municipalities and a post COVID world. Thanks

Thank you for your feedback. We really appreciate it. Have a great day!

Lisa C.

December 5th, 2023

Thank you. Very easy!

We are delighted to have been of service. Thank you for the positive review!

Linda K.

July 5th, 2019

This service was easy, quick, and to the point. It was a lifesaver! Downloaded quickly and without issues. I was able to fill out a soecifice form for my state and county, which saved me from making errors from a universal form.

Thank you for your feedback. We really appreciate it. Have a great day!

Eric M.

April 8th, 2021

Easy process and staff was very helpful

Thank you for your feedback. We really appreciate it. Have a great day!