California Trustee Deed Upon Sale

County Specific Legal Forms Validated as recently as July 21, 2026 by our Forms Development Team

About the California Trustee Deed Upon Sale

How to Use This Form

- Select your county from the list on the left

- Download the county-specific form

- Fill in the required information

- Have the document notarized if required

- Record with your county recorder's office

What Others Like You Are Saying

"No problem whatsoever navigating the forms. I hope the filing is this easy."

"AMazing service. Fast and affordable."

"Easy and Quick,Thanks"

"Easy and fast!"

"It works"

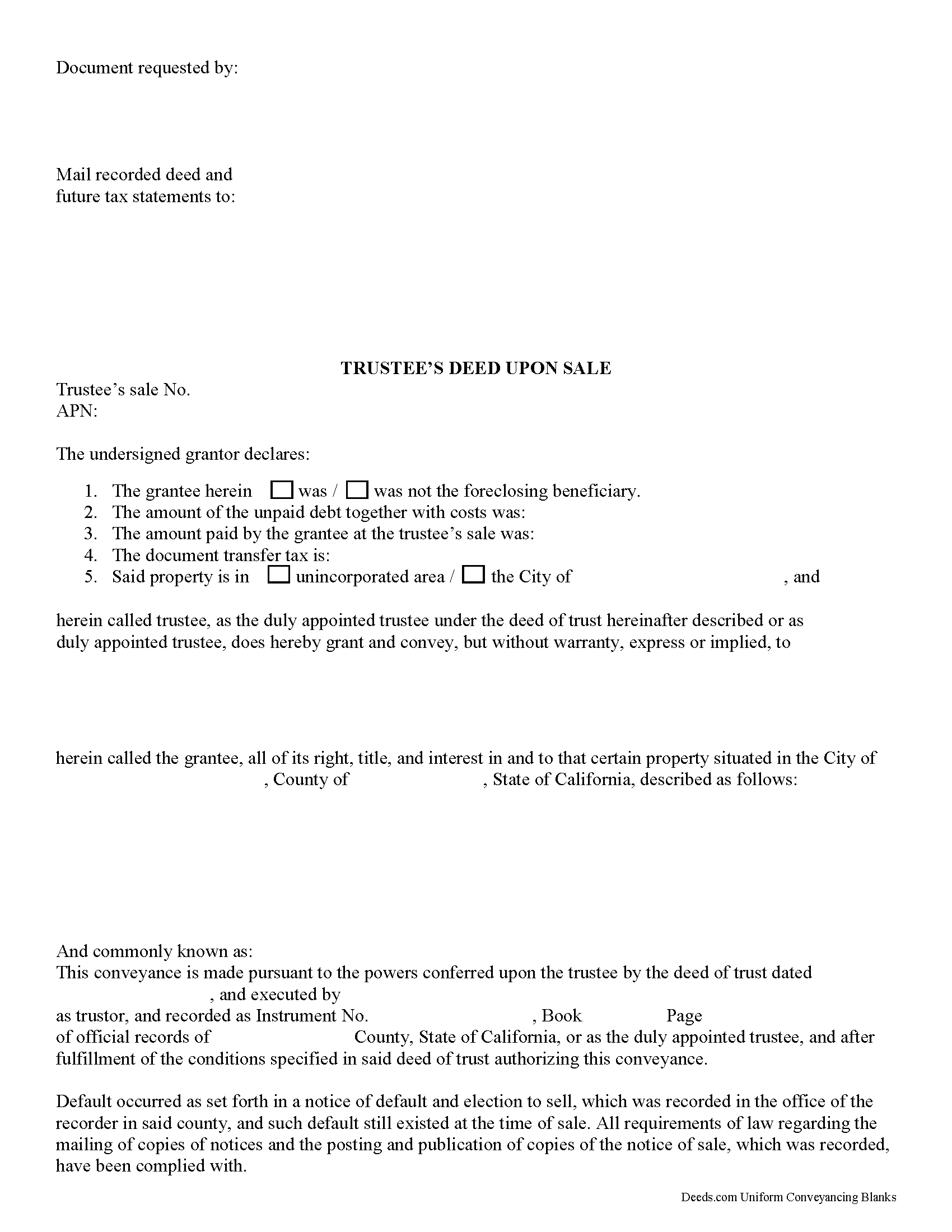

A California Trustee Deed Upon Sale is the conveyance used after a California deed of trust has been foreclosed through the state’s nonjudicial power-of-sale process. Buyers, foreclosing beneficiaries who credit bid, and trustees use this deed because the foreclosed owner does not sign a post-sale grant deed; the trustee conveys title under the authority in the deed of trust and California Civil Code section 2924. California’s form is different from many states because it must account for trustee-sale finality rules, one-to-four-unit residential bidder protections, and California’s unusual recording acknowledgment exception for trustee’s deeds from nonjudicial foreclosure (Cal. Gov. Code § 27287).

What a California Trustee Deed Upon Sale Does

A trustee deed upon sale confirms the transfer after the trustee has conducted a foreclosure sale under a deed of trust securing California real property. The deed typically identifies the trustor, trustee, beneficiary, recorded deed of trust, sale date, purchaser or grantee, vesting, consideration or credit bid information, and legal description. It is commonly used after a successful public auction, after the beneficiary acquires title through a credit bid, or after a residential trustee’s sale becomes final under California’s post-sale rules; it is not the same document as a deed signed by the trustee of a living trust.

California Statutory Requirements for the Trustee’s Deed

California’s nonjudicial foreclosure statutes control much of what a trustee’s deed upon sale must support in the recorded chain of title. The deed should be consistent with the completed foreclosure file and the public record of the deed of trust.

- Deed of trust parties. California treats the borrower as the trustor under a deed of trust and the secured lender as the beneficiary (Cal. Civ. Code § 2929.5(e)(1), (5)).

- Notice of default and sale foundation. The trustee, mortgagee, beneficiary, or authorized agent first records a notice of default in each county where the trust property, or part of it, is located, then proceeds through the statutory sale notice process after the required waiting period (Cal. Civ. Code § 2924(a)(1)-(4)).

- Power-of-sale recitals. A recital in the deed that the required mailing, publication, delivery, and posting steps were performed is prima facie evidence of compliance and becomes conclusive evidence in favor of bona fide purchasers and encumbrancers for value without notice (Cal. Civ. Code § 2924(c)).

- Sale finality and perfection. The trustee’s sale is generally deemed final when the trustee accepts the last and highest bid, and the sale is deemed perfected as of 8 a.m. on the actual sale date if the trustee’s deed is recorded within 21 calendar days after the sale. If an eligible bidder submits a written notice of intent to bid under section 2924m, the recording window for that retroactive perfection rule is 60 calendar days (Cal. Civ. Code § 2924h(c)).

- One-to-four-unit residential property. For real property containing one to four residential units, California delays finality in specified cases while eligible tenant buyers, eligible bidders, and prospective owner-occupants use the section 2924m process. The winning bidder’s affidavit or declaration, or the trustee’s statement that no affidavit or declaration is required, must be attached as an exhibit to the trustee’s deed and recorded (Cal. Civ. Code § 2924m(c), (d)).

- Attorney General reporting. When the winning bidder is an eligible bidder under section 2924m, the trustee or authorized agent must electronically send the specified sale information and a copy of the executed trustee’s deed, including the attached affidavit or declaration, to the California Attorney General within 15 days after the sale is deemed final (Cal. Civ. Code § 2924m(i)).

- Common interest development property. A transfer following foreclosure of property in a California common interest development must be recorded within 30 days after the date of sale in the county recorder’s office where the property, or a portion of it, is located (Cal. Civ. Code § 2924.1(a)).

Signing, Acknowledgment, and California Recording Format

The trustee named in the deed of trust, or a properly substituted trustee, signs the California trustee’s deed upon sale. The former owner or trustor does not sign this post-sale deed, and California does not require witnesses for this instrument. Unlike many recorded real-property deeds, a trustee’s deed resulting from a nonjudicial foreclosure under Civil Code section 2924 is excluded from Government Code section 27287’s acknowledgment prerequisite. When an acknowledgment is included, California’s all-purpose acknowledgment wording is controlled by Civil Code section 1189.

- First-page layout. California recording rules reserve the top 2½ inches of the first page for recorder use, with the left 3½ inches available for the recording requester and return address; documents that do not meet first-page requirements may need a cover sheet (Cal. Gov. Code § 27361.6).

- Document title. The first page should identify the instrument by title so the recorder can index it correctly as a trustee’s deed upon sale (Cal. Gov. Code § 27324).

- Party names. Names required for indexing must be legibly signed, typed, or printed, and record-title names must appear in the instrument when the document evidences a transfer or encumbrance (Cal. Gov. Code §§ 27280.5, 27288.1).

- Future tax statements. A deed conveying fee title must show the name and address where future tax statements should be mailed, typically on the first page (Cal. Gov. Code § 27321.5).

- Legal description and parcel number. The deed should include a complete legal description. California counties may require an assessor’s parcel number for tax administration, but the legal description controls over a conflicting parcel number (Cal. Rev. & Tax. Code § 11911.1(c)).

California Recording, Taxes, and County Forms

Record the trustee’s deed upon sale in the county recorder’s office where the California real property is located. Recording places the transfer into the public chain of title, and prompt recording matters because the 21-day and 60-day rules in section 2924h determine whether the sale is perfected back to 8 a.m. on the actual sale date. If the property spans more than one county, the recording package should account for every county in which a described portion of the property is located.

- Preliminary Change of Ownership Report. California generally requires a signed change-in-ownership statement when a change in ownership occurs. A Preliminary Change of Ownership Report is commonly submitted with the deed at recording; recordation is not denied solely because the statement is missing or incomplete, but separate assessor filing deadlines still apply (Cal. Rev. & Tax. Code § 480).

- Documentary transfer tax. California authorizes county documentary transfer tax on deeds when the consideration or value exceeds the statutory threshold, and cities may impose additional local transfer taxes (Cal. Rev. & Tax. Code § 11911).

- Foreclosure transfer tax treatment. A deed to a beneficiary or mortgagee taken as a result of foreclosure is not taxed up to the amount of the unpaid debt, accrued interest, and foreclosure costs; tax applies to consideration exceeding that amount. The deed or a separate affidavit or declaration should state the consideration, unpaid debt amount, and whether the grantee is the beneficiary or mortgagee when that exemption is claimed (Cal. Rev. & Tax. Code § 11926).

- Building Homes and Jobs Act fee. California’s additional recording fee under Government Code section 27388.1 can apply to real estate instruments, including trustee’s deeds, unless an exemption is available and properly claimed (Cal. Gov. Code § 27388.1).

California-Specific Recording and Title Traps

- Using the wrong recording window. Older California materials may refer to a 15-day trustee’s deed recording window, but the current section 2924h rule uses 21 calendar days, with a 60-calendar-day window when an eligible bidder submits a timely notice of intent under section 2924m.

- Missing the residential affidavit exhibit. For one-to-four-unit residential property, the section 2924m affidavit or declaration rules affect how the trustee’s deed is assembled. If no affidavit or declaration is required, the trustee’s statement that none is required must be attached as an exhibit to the deed (Cal. Civ. Code § 2924m(d)).

- Confusing deed-of-trust trustees with living-trust trustees. The trustee signing this deed acts under the power of sale in the recorded deed of trust. That role is different from a trustee managing a living trust for estate-planning purposes.

- Importing another state’s homestead language. California homestead rules do not create a separate spouse-signature or homestead-waiver block on a trustee’s deed upon sale. The trustee, not the foreclosed owner or the owner’s spouse, executes the post-sale conveyance.

- Adding unnecessary marital status recitals. California does not require the foreclosed trustor’s marital status to be recited as a grantor-signature requirement on this deed because the trustor is not the signing grantor. Marital wording matters for the grantee’s vesting when spouses take title in a California survivorship form.

- Treating the APN as the legal description. The assessor’s parcel number helps the county identify tax records, but it does not replace the legal description. For subdivided property, the legal description may need lot, tract, map book, and page references from recorded maps.

- Omitting transfer-tax exemption details. A trustee’s deed to the foreclosing beneficiary is not automatically exempt from every transfer-tax calculation. Section 11926 exempts the amount tied to the unpaid debt, accrued interest, and foreclosure costs, while excess consideration can remain taxable.

- Confusing preparer information with California first-page information. California does not use the same statewide deed-preparer statement found in some states. The common California recording focus is the recording-requested-by space, return address, tax statement address, title, margins, and indexing information.

Vesting the Grantee in California

A trustee’s deed upon sale places title in the grantee’s name, so the vesting language should match California ownership terminology. California recognizes several forms of ownership by more than one person, and survivorship is not presumed from co-ownership alone (Cal. Civ. Code § 682).

- Tenancy in common. Co-owners may hold separate undivided interests without a survivorship feature.

- Joint tenancy. A California joint tenancy must be expressly declared in the transfer document (Cal. Civ. Code § 683).

- Community property with right of survivorship. For spouses, this vesting must be expressly declared in the transfer document and accepted in writing on the face of the deed by the grantees’ signatures or initials (Cal. Civ. Code § 682.1).

What Is Included in the California Trustee Deed Upon Sale Download Package

The download package is prepared by Deeds.com’s forms development team for California trustee’s deeds upon sale and is designed for use with county recording requirements.

- California Trustee Deed Upon Sale form

- Line-by-line instructions for completing the trustee, beneficiary, trustor, sale, grantee, vesting, tax, and legal-description sections

- Completed example showing how a California trustee’s deed upon sale is commonly assembled

- Guidance on California recording details, including first-page formatting, tax statement address, documentary transfer tax declaration, Preliminary Change of Ownership Report, and section 2924m attachments when applicable

How to Use This Form

- Select your county from the list above

- Download the county-specific form

- Fill in the required information

- Have the document notarized if required

- Record with your county recorder's office

What Others Like You Are Saying

"No problem whatsoever navigating the forms. I hope the filing is this easy."

"AMazing service. Fast and affordable."

"Easy and Quick,Thanks"

"Easy and fast!"

"It works"

Compare with related California forms

Important: County-Specific Forms

Our trustee deed upon sale forms are specifically formatted for each county in California.

After selecting your county, you'll receive forms that meet all local recording requirements, ensuring your documents will be accepted without delays or rejection fees.